The Friday Alaska Landmine column: There is no conflict between SB 26 and the PFD statute

SB26 & the PFD fit together fine, yet some who claim "rules-based" is critical when focused on the POMV do cartwheels to ignore the one in place for the PFD. Why is that?

One of the claims we sometimes hear from those seeking to rationalize legislative cuts in the statutory Permanent Fund Dividend (PFD) is that there is a “conflict” between SB 26 – the statute enacted in 2018 setting limits on overall draws made from the Permanent Fund at a percent of market value (POMV) – and the statute governing the PFD, and thus, the Legislature annually “has” to make a choice between the two.

That’s not true. While applying both as written would require the Legislature to make some additional decisions more transparently, there is no actual conflict between the two. The claim of a “conflict” is merely a cover story used by those who want to further obfuscate the nature of the decisions they are making about who pays for the costs of government.

Because they both govern draws from the Permanent Fund earnings reserve, the statutes governing the POMV and PFD are generally intertwined in the same two sections of the Alaska statutes: AS 37.13.140 and AS 37.13.145.

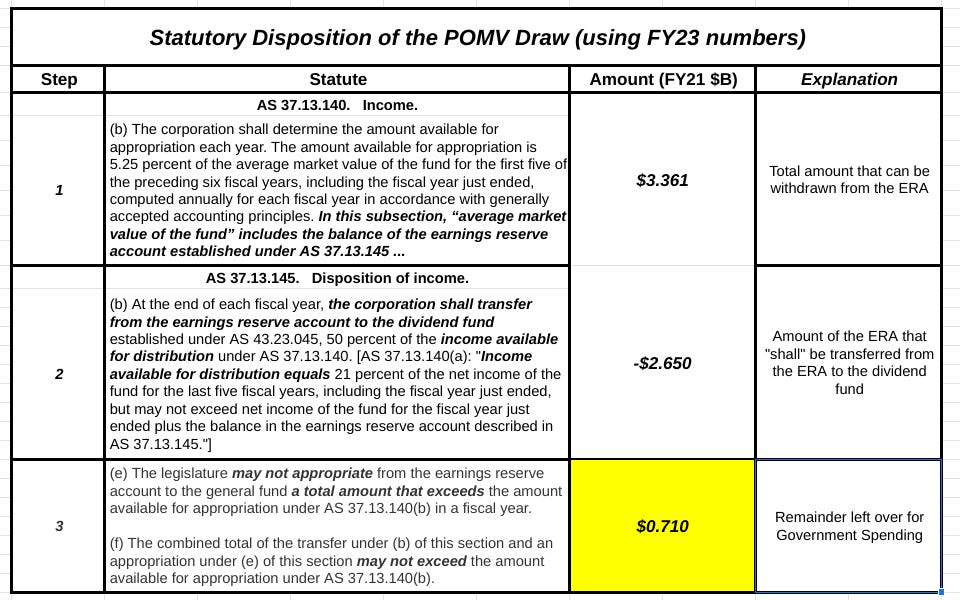

The framework for the overall POMV draw is set by AS 37.13.140(b) and AS 37.13.145(e) and (f). Within that, the PFD is governed by AS 37.13.140(a), AS 37.13.145(b) and also to some degree, AS 37.13.145(e) and (f).

(For those interested, AS 37.13.145 also deals with establishing the Permanent Fund earnings reserve (AS 37.13.145(a)), providing for an annual inflation adjustment (AS 37.13.145(c)) and handling what are referred to as the “Amerada Hess” funds (AS 37.13.145(d)).)

The key to understanding why there is no conflict is to appreciate that, while there is a statutory provision – a rule – which designates a specific amount from within the overall POMV draw to be set aside for the PFD, there is no provision which similarly designates a specific amount to be used to help pay for government spending.

Thus, this isn’t a case where the statutes say “3” shall be used to fund the PFD, “3” shall be available for government spending (or “6” total), when there’s only “5” available.

Rather, the statutes say “3” shall be used to fund the PFD, and you can use the POMV draw also for government spending, but can only withdraw “5” total

As a result, if there is a “leftover” argument to be made from the statutes, its that the amount available to pay for government spending is what’s leftover from the overall POMV draw after the amount set aside for the PFD has been transferred “to the dividend fund established under AS 43.23.045.”

The provision which designates the specific amount to be set aside for the PFD is at AS 37.13.145(b). That subsection reads as follows:

(b) At the end of each fiscal year, the corporation shall transfer from the earnings reserve account to the dividend fund established under AS 43.23.045, 50 percent of the income available for distribution under AS 37.13.140.

The provision which governs the use of the POMV draw to help pay for government spending is at AS 37.13.145(e). Because that subsection applies to both the amounts used for the PFD and the amounts to be used for government spending (both of which are part of the “general fund”), however, it does not set aside a specific amount for government spending. Rather, it sets a ceiling on the combined amount:

(e) The legislature may not appropriate from the earnings reserve account to the general fund a total amount that exceeds the amount available for appropriation under AS 37.13.140(b) in a fiscal year.

This ceiling is then reinforced by AS 37.13.145(f), which provides as follows:

(f) The combined total of the transfer under (b) of this section and an appropriation under (e) of this section may not exceed the amount available for appropriation under AS 37.13.140(b).

Some become confused about the relationship between the POMV and PFD draw because they involve different calculations. The overall POMV amount is calculated based on “the amount available for appropriation each year” determined in accordance with AS 37.13.140(b). The PFD draw is calculated based on “Income available for distribution” determined in accordance with AS 37.13.140(a).

While they may sound the same, they aren’t. The “amount available for appropriation each year” used in the calculation of the POMV draw is based on the “average market value of the [Permanent] fund” for the preceding five fiscal years. On the other hand, the “income available for distribution” used in the calculation of the PFD draw is based on the “net income of the fund” for the last five fiscal years, “including the fiscal year just ended” at the time the distribution is made.

In short, one is asset (value) based, the other is income based and they apply to slightly different time periods.

But that doesn’t create a conflict. They are merely different ways of calculating the amounts involved.

Some also point to a difference between the use of the word “transfer” in connection with the PFD and “appropriate” in AS 37.13.145(e) as the basis for a conflict. But as the Supreme Court’s 2017 decision in Wielechowski v. State makes clear, in the context of Alaska fiscal law the word “transfer” is nothing more than a synonym for “appropriation.”

As a result, taken together, this is how the statutes are set up to operate, as written:

… or put graphically, this:

Some nonetheless seek to cloud the operation of the statutes as written because of their significant impact on discussions about government spending.

For example, looking at the FY22 budget (as enacted, before supplementals), here is the result of applying the POMV and PFD statutes as written:

Applying the POMV and PFD statutes as written shows that unrestricted general fund (UGF) spending is substantially outstripping statutory revenues and that additional funds are required, not to pay the PFD, which is adequately covered by the draw from the earnings reserve, but to cover the deficit created by the imbalance between total UGF revenues available for government and total UGF spending.

While the Supreme Court’s decision in Wielechowski makes clear that PFD cuts can be the source of some (or all) of the additional funds through appropriation, at least looking at the issue as statutorily constructed makes clear what is going on if they are: middle and lower income Alaska families – who, “by far,” are most impacted by PFD cuts – are being targeted to bear the brunt of the additional funds required to cover the costs of general government spending.

In short, Peter is being required largely to pay for both Peter’s and Paul’s shares of the additional costs of general government spending which benefits all Alaska families.

On the other hand, by ignoring the statute (or arguing that there is a “conflict” and so, the Legislature “has” to choose), those wishing to rationalize PFD cuts seek to present the issue differently, like this:

By ignoring (or more accurately, misrepresenting) the statute, they argue that the need for any additional funds required to balance the budget is not being caused by general government spending, which they claim already is adequately covered by UGF revenues, but the PFD.

They then turn that into a claim that adopting any “new” taxes would be to pay for a higher PFD, not to fund general government spending.

In that way they seek to change the discussion from one focused on what is the fairest and lowest impact (economically) way to raise the additional funds needed to pay for general government spending, to one focused instead, as Senator Natasha von Imhof (R – Anchorage) once phrased it, on the alleged “greed” of those Alaskans seeking to protect the PFD.

By phrasing the issue differently, they seek to obfuscate the decision they are making to push the burden of general government spending largely onto the backs of middle and lower income – 80% of – Alaska families, allowing the top 20% to escape by contributing only a trivial amount.

Ironically, in the effort many who emphasize the importance of observing the statutory “rules-based” system when focused on the overall POMV draw, quickly abandon the already existing statutory rules and claim chaos when it comes to allocating that draw between the PFD and support for government spending.

Given the Wielechowski court’s decision that the Legislature can appropriate funds designated for the PFD to other purposes, the two approaches may end up in the same place anyway – and indeed they have for the last six years – but at least it should happen based on a fair reading of Alaska’s statutes – and the policy choices that they represent – rather than some twisted, manipulated version designed to obfuscate the decisions being made behind the scenes in crafting Alaska’s budget.