The Friday Alaska Landmine column: It’s the revenues, stupid

Adapting the old James Carville mantra, we explain why the key catchphrase this coming Alaska legislative election cycle should be "It's the revenues, stupid"

To those of a certain age, one of the most memorable pieces of past campaign strategy is the mantra developed by advisor James Carville for those working on then-candidate Bill Clinton’s 1992 presidential campaign. To keep the campaign on message, Carville hung a sign in Clinton’s Little Rock campaign headquarters that read, in part: “It’s the economy, stupid.”

That mantra comes to mind as we begin to consider the fiscal policies proposed by this year’s field of legislative candidates. Except this year, our mantra in evaluating the positions will be “It’s the revenues.”

We realize that some will immediately take issue with the focus, arguing, “No, it’s not; it’s the spending.”

But while that may have been true at one time, the Legislature – Republicans and Democrats/Independents alike – has long since passed the point of no return on that issue.

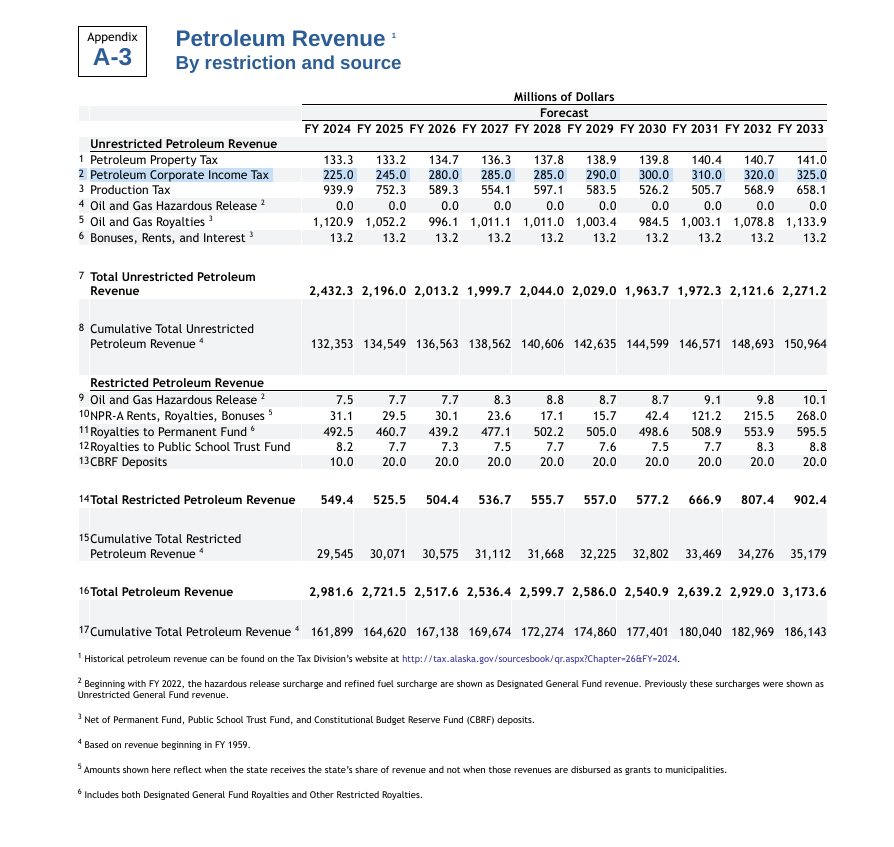

As we discussed in last week’s column, the unrestricted general fund (UGF) spending level this Legislature just sent to the Governor for consideration totals around $5.5 billion. Looking at the Department of Revenue’s Spring 2024 Revenue Forecast (Spring Revenue Forecast), the very best year in terms of current law revenues over the next eight years is $4.7 billion. The average over the period is $4.3 billion.

To match that – for this election not to be about “it’s the revenues” – UGF spending would need to be ramped down by nearly 22% (roughly $1.2 billion) immediately in the next legislative session and held absolutely flat at that level over the remaining eight years to balance at projected current law revenue levels. Even those who didn’t live through Governor Mike Dunleavy’s (R – Alaska) failed effort to do something similar in the 2019 legislative session will quickly realize that’s just not going to happen.

In our view, any legislative candidate who runs on a platform of resolving Alaska’s fiscal situation through “spending cuts only” should be immediately dismissed as irredeemably naive.

Some may alternatively claim that the situation will resolve itself if we can just hold out until new oil production comes online from Santos’ Pikka and Conoco’s Willow projects. Indeed, a recent op-ed in the Anchorage Daily News went so far as to imply that those projects are on track to produce a “revenue windfall” sufficient to fund a second Permanent Fund.

But that’s also not true.

The numbers in the chart above already include the revenues anticipated to result over the period from the projected production increases coming from Pikka and Willow. Here is the breakdown:

While production volumes are projected to rise by over 36% over the eight-year period (an annual compound growth rate of 4%), total petroleum revenues from those volumes are projected to rise over the period by only 3% in total (an annual compound growth rate of 0.4%).

Even more startling for those hoping to make the claim, revenues from production taxes and oil and gas royalties – the two sources most closely tied to production levels – are projected to decline over the period by 0.7% (an annual compound growth rate of minus 0.1%). (We discussed the reasons why in a previous column.)

According to the Spring Revenue Forecast, the only oil-related component projected to rise over the period at a rate equal to or faster than that forecast for spending growth by the Legislative Finance Division (a highly conservative annual rate of 2.5%) is revenues from the petroleum corporate income tax. Those are forecast to rise by nearly 33% over the period, or at an annual compound growth rate of 3.6%. But those only account for 14% of overall UGF petroleum revenues and, ironically, are the revenue source that Hilcorp, the state’s second-largest producer, currently avoids due to its corporate structure. The projected level of growth there doesn’t even begin to offset the decline and subpar performance from the other components.

For those interested, here is the detail behind the numbers:

In short, there are no dodges. To be taken seriously this election cycle, at least by us, legislative candidates must discuss revenues.

In response, we anticipate some will quickly say, as the Senate proposed in SB107, “Restructuring (cutting) the Permanent Fund Dividend (PFD) to POMV (percent of market value) 25/75.”

But as we’ve explained in previous columns, that’s no more than code for saying, “Through continued and additional taxes on (or if you prefer, “reductions in income” to) middle and lower-income Alaska families while letting the top 20%, non-residents, and the oil companies off the hook.”

Those genuinely concerned about the decline in the number of working-age Alaska families and the impact of a growing, government-induced income gap between upper-income families on the one hand and middle and lower-income (80% of) Alaska families on the other, as well as the hugely adverse impact of a regressive fiscal policy on the overall Alaska economy, should dismiss those giving that response as quickly as they should those saying “spending cuts only” or “production growth.”

Moreover, as well as being anti-family and anti-economy, the usefulness of that response evaporates quickly. Even if spending is held to an annual growth rate of 2.5%, it quickly outstrips overall revenue (calculated at POMV 25/75), which is growing at less than 2%. Using the $5.5 billion spending level approved by the Legislature this session as a base, the budget is already back in deficit beginning next year – the first that the Legislature elected this year will address – even at POMV 25/75.

As a result, having started down the road by already agreeing to POMV 25/75, those making that argument this campaign seem essentially to be signaling that beginning next year, they are prepared to vote to tax middle and lower-income Alaska families at hugely regressive rates even higher than the so-called POMV 25/75 approach in an effort to continue to stave off taking more than a trivial share from the top 20%, and none from non-residents and oil companies.

In short, they seem prepared to continue to tax middle and lower-income families at rates even beyond the levels resulting from POMV 25/75 in order to continue to protect those in the top 20% from paying more than a trivial share and non-residents and oil companies zero.

Maybe others will, but we certainly won’t be supporting any candidates taking that position.

Thus, the question this cycle to serious legislative candidates isn’t “if,” it’s what type of alternative revenue measures they are prepared to endorse.

To us, the answer is a combination of three things: closing the Hilcorp loophole, adjusting oil production taxes, and a broad-based tax that reaches the top 20% and non-residents to cover the remainder of the deficit.

Closing the Hilcorp Loophole should be a no-brainer. As every revenue forecast makes clear, the Alaska petroleum tax code currently uses five components to raise unrestricted revenues: Petroleum Property Tax, Petroleum Corporate Income Tax, Production Tax, Oil and Gas Royalties, and Bonuses, Rents, and Interest.

Like any well designed tax code, the reason Alaska’s petroleum tax has different components is to ensure that overall revenues from the resource remain at least somewhat stable regardless of the circumstances at the time. Just as is projected to occur over the next eight years, for example, when revenues from one source – e.g., production volumes – are stagnating or in decline, taxes calculated using other components – e.g., property and corporate income – may serve to provide some offset.

The petroleum corporate income tax – the state’s third largest unrestricted revenue source from petroleum – was designed at a time when all of the major oil companies operating in the state – as well as most elsewhere in the United States – were structured as so-called “C” (after a provision of the federal Internal Revenue Code) corporations. Continuing that approach in a changing corporate structural environment worked well, however, only until BP (a “C” corporation) sold its Alaskan interests to Hilcorp. Because Hilcorp was structured slightly differently (as an “S” corporation), it fell outside the scope of the existing petroleum code. It’s not – as some have claimed – that the petroleum code intentionally provided an exclusion for S corporations; it’s simply that, because all of Alaska’s major oil companies were formed and had been operated as “C” corporations, there was no need to update the state’s petroleum tax code even as “S” corporations became more popular elsewhere.

The failure to update the Alaska statute once one of the corporations producing a major share of the state’s oil resources became an S corporation, however, has meant that, unlike the other major oil corporations operating in the state, Hilcorp has been able to avoid the third largest component of the state’s overall petroleum tax code. There is no reasonable policy explanation for the exclusion, and it should be closed by finally updating the state’s petroleum tax code also to include oil companies – at least those holding a significant share of the state’s production – structured as “S” corporations.

As the following chart reflects, the result would be to increase unrestricted petroleum revenues over the period by roughly $120 million, or 5% annually.

Adjusting oil production taxes is also needed. As we have explained in previous columns, consistent with the state’s Constitution, the overall goal of Alaska’s oil code should be to maximize the revenue received for the state’s oil resources. Despite efforts by others to suggest differently, that approach is entirely consistent with the goal also of making the state “competitive” for oil investment dollars.

As we discussed in those columns, taxing at a level that discourages oil investment easily could backfire by reducing revenues to levels lower than those achieved at lower tax rates but higher investment and, as a result, production levels. But that doesn’t mean that the state should set taxes at artificially low levels to ensure that it continues to attract a given level of investment.

Instead, the state should strive for the proverbial “just right” approach, setting tax and other revenue rates at the “revenue-maximizing” level – just high enough to produce all the revenues that the state can receive from the resource without pushing investment levels down to the point that the state’s revenue levels start to decline.

As we have explained in those columns, we believe Alaska’s production tax is currently falling significantly short of that level. Oil industry economics have changed materially in the decade since the state’s production tax approach was last reset. In the recent past, even the Dunleavy administration’s Department of Revenue has seemed to admit that oil tax levels can be increased to some extent without adversely impacting production levels.

As we explained in a column last month, while we don’t believe that even combined with closing the Hilcorp Loophole, raising oil taxes to their “revenue-maximizing” level is sufficient, standing alone, to offset the entire current law deficits the state is facing, we do believe that they are a significant part of any answer and should be part of any serious candidate’s platform to address Alaska’s fiscal situation.

Finally, adopting a broad-based tax should also be part of the fiscal position adopted by any serious candidate. As we have explained repeatedly in these columns, Alaska families are already being taxed to help balance the state’s budget. Indeed, as Dr. Matthew Berman, a Harvard and Yale-trained, long-time Professor at the University of Alaska-Anchorage Institute of Social and Economic Research (ISER), has explained, through PFD cuts, Alaskan families are incurring the “the most regressive tax ever proposed.”

The problem with that approach is legion. It focuses the burden only on Alaskan families. Unlike in every other state in the nation, non-residents engaged in some form of commercial activity in Alaska contribute zero toward the costs of state government. As a consequence, Alaskan families bear a materially greater burden than they would if it was spread more broadly to include non-residents.

The approach is hugely regressive, meaning it has a much greater impact on middle and lower-income Alaska families than on those in the upper-income brackets. Through this step alone, the Legislature artificially is widening the income gap in the state between upper and working-class Alaska families, and, by pushing additional costs down on working-age middle and lower-income Alaska families, appears also to be contributing to the state’s significant migration problem in that sector.

Through those effects, the approach also has an adverse impact (indeed, according to a 2016 study by ISER researchers, the “largest adverse impact” of all the various revenue options) on the overall Alaska economy.

And, by taking only a trivial share of income from those in the upper-income brackets, the approach seriously reduces, if not eliminates, their “skin in the game” in terms of state spending levels and, with it, their incentive to help find a reasonable balance between those levels and the revenues required to pay for them. Under the current approach, more government programs essentially are a “free good” to them. As with any free good, their reaction is either indifference at best or, more likely, “the more spending, the better.”

These create deeply serious problems for both the vast majority (80%) of Alaska families and the overall Alaska economy, which we believe every candidate for the Legislature should address this cycle by offering a broad-based revenue source to substitute for and replace the continued use of PFD cuts.

Conservative candidates may prefer suggesting a sales tax similar to Representative Ben Carpenter’s (R -Nikiski) proposed HB 142. While still regressive, the approach is a vast improvement over even more deeply regressive PFD cuts.

Moderate and progressive candidates may prefer suggesting progressive income taxes, which scale up from the minimalist and, thus far, woefully insufficient proposals made by Reps. Alyse Galvin (I – Anchorage) and Zack Fields (D – Anchorage).

For our part, we prefer a flat tax along the lines analyzed for the Legislature in 2021 by the Institute on Taxation and Economic Policy (ITEP) and generally supported at a state level nationally by the Tax Foundation. We support that approach not only because it takes no more from any one Alaska family than any other but also because it ensures that all Alaska families and industries relying on non-residents have an equal incentive to seek an overall balance between spending and revenues.

But whichever approach they adopt, all candidates should take a realistic, intelligible, and balanced approach to the problem to demonstrate their understanding of the seriousness of the state’s fiscal situation and the consequences of continued reliance on PFD cuts.

In this cycle, the mantra needs to be, “It’s the revenues, stupid.” Candidates who dodge the issue – or address the issue only in ways that continue to push the burden off primarily on middle and lower-income Alaska families – should be left behind.