The Friday Alaska Landmine column: A relook at sales taxes

By significantly broadening the base, Rep. Ben Carpenter's proposed sales tax lowers the current level of govt take on nearly all Alaska households. His opponent should endorse it, not criticize it.

Over the years, we have been less than supportive of using a statewide sales tax to help address Alaska’s fiscal deficits. While certainly not as regressive as using cuts in the Permanent Fund Dividend (PFD), sales taxes are still regressive. As the 2017 report for the then-legislature by the Institute on Taxation and Economic Policy (ITEP) explained:

… sales taxes tend to be regressive, impacting low- and middle-income families more heavily than high-income families when measured as a percentage of household income. This effect comes about largely because low- and middle-income families spend a larger fraction of their earnings on items subject to sales tax, while high-income families direct a large share of their income into savings and investments.

As part of their study, ITEP was asked to look at a proposal that was then considered by the Department of Revenue. The proposal, designed to raise $500 million in revenue, was “a 3 percent sales tax … [that] would include exemptions for various necessities such as groceries, health care, prescription drugs, shelter, and child care.” Even with the exemptions, ITEP concluded: “that the tax would be regressive overall, requiring payments from low-income Alaskans equal to roughly 2.2 percent of their incomes compared to 1.5 percent for middle-income families and 0.4 percent from the state’s top 1 percent of earners.”

Recently, however, we have started to moderate our concerns as we have dug deeper into a bill introduced this past Legislature by Representative Ben Carpenter (R – Nikiski) as part of an overall package that is, in part, an outgrowth of the then-legislature’s 2021 Fiscal Policy Working Group. We started digging into the bill – HB 142 – because of some blatant misrepresentations being made about Representative Carpenter’s efforts by Senator Jesse Bjorkman (R – Nikiski), who Carpenter is challenging this election cycle.

Bjorkman is attacking Carpenter over Carpenter’s proposed sales tax as if it is a standalone measure to be layered on top of existing revenue sources.

But it’s not. The sales tax is only one component of a larger package of bills designed to be revenue-neutral overall. Other parts include restoring the Permanent Fund Dividend (PFD) to a level based on distributing 50% of the annual percent of market value (POMV) draw from the Permanent Fund (the so-called “POMV 50/50” approach) instead of the POMV 25/75 approach currently used by the Legislature, putting the PFD in the Constitution to avoid later, ad hoc legislative cuts, a robust spending cap to limit state spending, and a revamp of the state’s corporate income tax designed to make Alaska more competitive in its efforts to attract expanded corporate activity.

In the context of the total package, the sales tax serves two purposes. First, it largely serves as a replacement for cuts in the PFD between POMV 50/50 PFD and POMV 25/75. Second, it serves as a replacement for the proposed corporate income tax cuts. In both roles, it is a replacement for current revenues, not an addition. And it is largely protected from further growth by the spending cap. There is currently no such protection for continued growth in PFD cuts or corporate taxes.

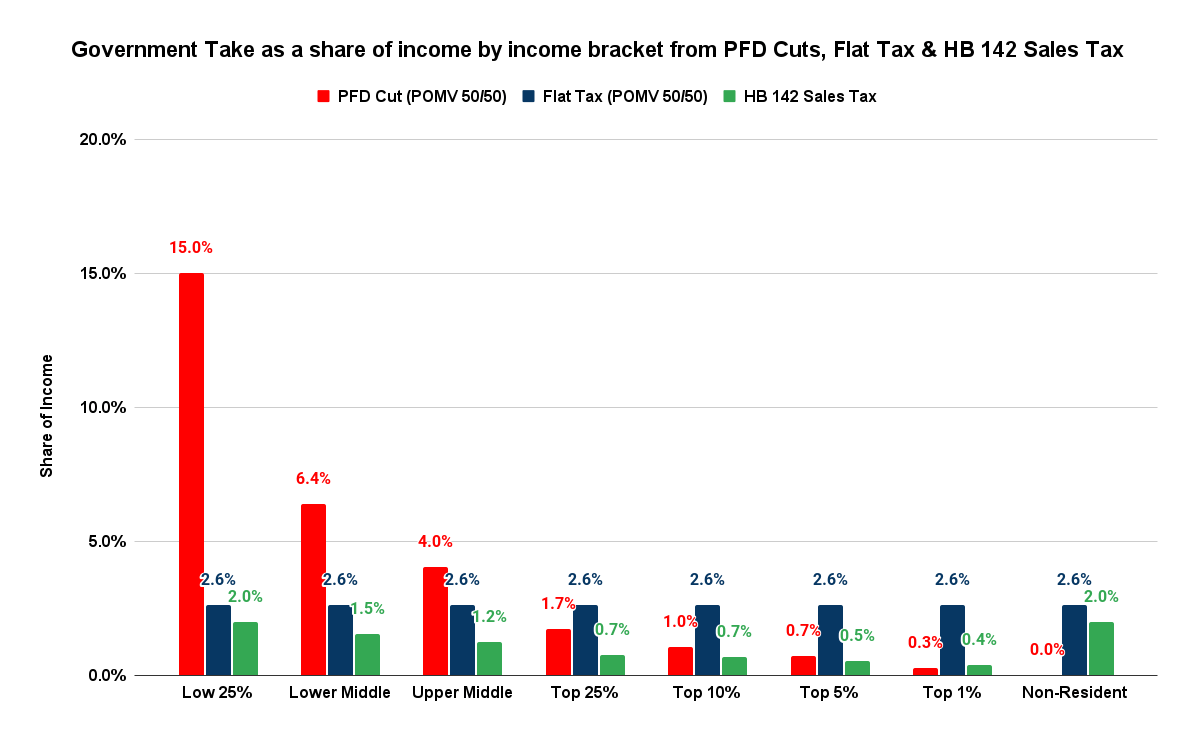

Measured by the portion used, the primary purpose of the sales tax is as a replacement for deeper PFD cuts. Averaged over time, this purpose explains about $1 billion – or about two-thirds – of the $1.5 billion in annual revenue to be raised by the HB 142 sales tax projected in the accompanying fiscal note. The remainder is used to offset the corporate income tax cut.

Put another way, roughly 1.3% of the sales tax goes toward reducing the future level of PFD cuts. The remaining 0.7% goes toward reducing the level of corporate taxes.

What we have realized as we have dug deeper into the bill is that even counting the entire 2%, the HB 142 approach takes less from middle and lower-income Alaska families not only than PFD cuts, which we already knew, but also than the flat tax we have long advocated. Here is the distributional effect based on the full amount of the sales tax compared to the impact of the portion of PFD cuts it is replacing:

While the HB 142 sales tax would still be regressive – take more from middle and lower-income Alaska families than those in the upper-income bracket – it would take less from those same families than even a flat tax. Even including the portion designed to cover the reduction in the corporate income tax, the combined amount is still lower than using a flat tax to cover only the portion attributable to the PFD cuts. Put another way, the full 2% sales tax is still less than the 2.6% flat tax.

Alaskan families would pay less.

How does the HB 142 sales tax do that? To paraphrase – and misspell – an early 2010s pop song, “it’s all about the base.”

As we explained above, at full implementation, the HB 142 sales tax is estimated to raise about $1.5 billion annually. Doing the arithmetic, that implies a tax base of roughly $75 billion ($75 bn x .02 = $1.5 bn). On the other hand, Alaska adjusted gross income, adjusted for a POMV 50/50 PFD and income received in Alaska by non-residents, will likely average only around $40 billion over the same period.

The math is simple. Raising even $1.5 billion from a tax base of $75 billion takes less as a share of income from Alaska families than raising $1 billion from a tax base of $40 billion.

Why is the sales tax base so much larger? Because, in addition to purchases made by Alaska families, it includes purchases of goods and services in Alaska made by tourists, non-residents, businesses, and others. As described in the fiscal note:

This bill would impose a statewide sales and use tax of 2 percent on the sale or lease of tangible personal property, the sale of services, and the use of tangible personal property or services that would be subject to the tax if purchased in the state. The tax base in this bill is considered to be a “high base” tax base in that the bill does not include exemptions for business‐to‐business transactions, groceries, medical equipment, or medical services.

In short, the sales tax would redirect elsewhere a significant share of the burden otherwise currently being borne entirely by Alaska families – and primarily middle and lower-income Alaska families – using PFD cuts.

HB 142 also has a larger base than previous sales tax proposals. The 3% sales tax, with exemptions, discussed in the 2017 ITEP study was designed to raise $500 million, implying a tax base of $16.7 billion. The various sales tax proposals surfaced by the Department of Revenue (DOR) in 2020 and 2021 imply tax bases of between $15 billion (4% state sales tax styled on Wyoming sales and use tax) and $32 billion (4% state sales tax styled on South Dakota sales and use tax).

We opposed each of those because the size of the base was not sufficient to offset the adverse impact on Alaska families. Besides regressive, the proposed sales tax took more from middle and lower-income Alaska families than a flat tax approach.

The ultra-broad base used by HB 142 changes that. As demonstrated in the chart above, the HB 142 sales tax takes less from middle and lower-income Alaska families than even a flat tax approach. What some view as a defect in HB142 – the lack of exemptions – is, in fact, a feature. By broadly expanding the base, the approach reduces the take from Alaska families to a lower level than if the base was narrowed by exemptions and exclusions.

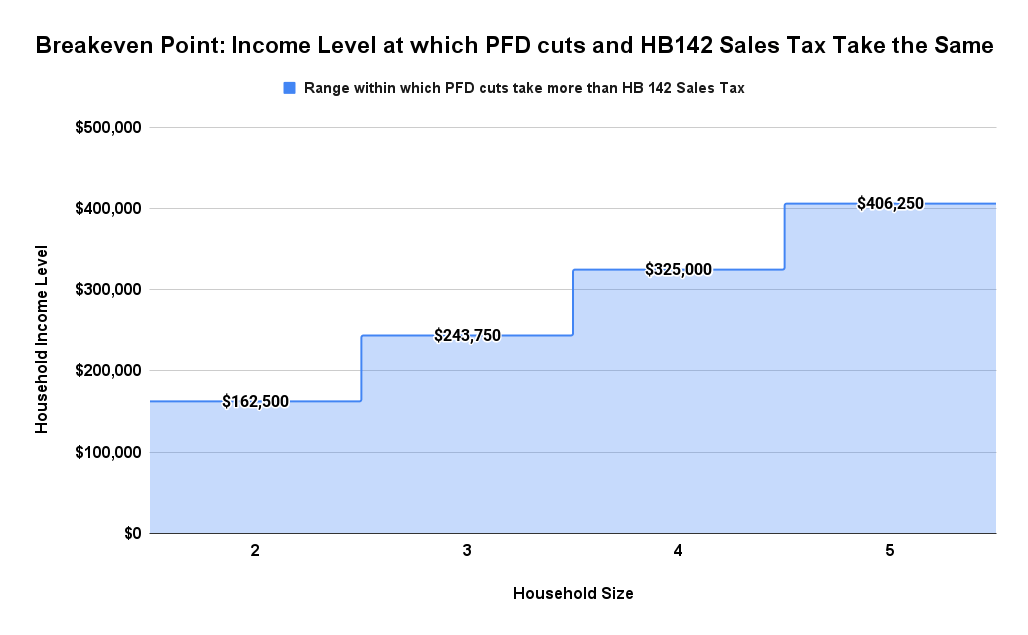

Another way to compare the HB 142 sales tax and PFD cuts is to look at the breakeven points – the point at which each approach takes the same as a share of income.

The points can be somewhat complex to calculate. As ITEP noted, the impact of a sales tax as a share of income decreases as income rises because, at higher-income levels, more is directed into savings and investments, a use of income not subject to the tax. Calculating the detailed breakeven points requires taking that so-called “marginal propensity to save” into account.

As the following charts demonstrate, however, we can see the breakevens are high even before adjusting for the marginal propensity to save.

For a household with two residents, using PFD cuts to raise $1 billion in additional revenue reduces household income by roughly $3,250 ($1,625 x 2 = $3,250). Even if all that income is spent on purchases subject to a 2% sales tax, a household doesn’t incur the same level of government take until income reaches $162,500 ($162,500 x .02 = $3,250). Households of two are better off with a sales tax – the government take is smaller – at all income levels below that level. For example, if household income is $100,000, the level of government take from the sales tax is only $2,000, less than the $3,250 from PFD cuts.

The remainder of the chart shows the breakeven levels at households with three, four, and five residents. The breakeven point rises because the aggregate level of the PFD cuts grows larger due to the increased number of residents.

Factoring in the marginal propensity to save pushes the breakeven points even higher. For example, the breakeven point for a household of two that, on average, saves or invests 10% of its income is approximately $180,555. At 10%, the amount saved or invested is $18,055. Even if the remaining $162,500 is spent on purchases subject to a 2% sales tax, the tax is still only equal to the $3,250 taken through PFD cuts.

Despite our overall support, however, there is one aspect of HB 142 we question. As we explained above, about a third of the 2% sales tax is being used to offset reductions in the corporate income tax. Using that, instead, to substitute for additional PFD cuts would have the effect of restoring the PFD to full statutory levels. On the other hand, reducing the sales tax to around 1.3% and foregoing the portion used to offset reductions in the corporate income tax would still be sufficient to restore the PFD to POMV 50/50.

Our question is whether using a sales tax to cover corporate income tax reductions is the best use of the funds. It may be that the increased economic activity in Alaska resulting from reducing the corporate income tax will more than make up for the impact of that portion of the sales tax. We have yet to see that case persuasively made, however, and believe there should be more analysis quantifying the impacts, both positive and negative, before committing to that approach.

We are mindful of the old aphorism, however, to avoid allowing the perfect to become the enemy of the good. As we have explained above, even at a 2% rate, the ultra broad-based sales tax created by HB 124 takes less from middle and lower-income – in total, 80% of – Alaska families than do the incremental PFD cuts or even a flat tax associated with a POMV 25/75 PFD cut.

Yes, it might be better still from that perspective if the full amount of the sales tax was used instead to replace any cuts to the statutory PFD or if the sales tax rate was reduced to 1.3%. However, we need to remember that it’s still a good deal for the vast majority of Alaska families, even if the final rate is 2%, and a portion of it is used to replace some reductions in the corporate income tax.