The Friday Alaska Landmine column: Is Alaska on its way to mimicking Venezuela?

After listening to the recent legislative hearing on the Cook Inlet gas market, we wonder whether Alaska is on its way to mimicking Venezuelan energy policy. We explain why and why that's a concern.

While following the Joint Senate and House Resources Committees meeting on Cook Inlet gas last week, we suddenly realized some of those testifying were proposing that the Legislature consider adopting an energy policy similar to Venezuela.

Certainly, no one in the hearing made that analogy, but the parallel became very apparent while listening to some portions of the testimony from John Sims, the president of Enstar Natural Gas. This is how blogger Matt Buxton, who was live tweeting the discussion, put what Sims was saying:

The implication was clear: Sims was suggesting that the state provide some form of tax “cuts” (or royalty “cuts,” since the Cook Inlet producers largely don’t pay taxes) to producers – in effect, subsidies by the state to those producers – so those producers would, in turn, reduce the cost of gas to the Cook Inlet gas buyers, and through them, to consumers.

This reminded us immediately of Venezuela, where the government subsidizes the cost of gasoline to keep the price to consumers low.

Generally speaking, most free-market observers condemn that approach, arguing that it leads to unintended consequences, such as significant budget deficits and shortages of gasoline supplies due to artificially inflated demand. We think there would be some similar consequences here from what Sims is suggesting.

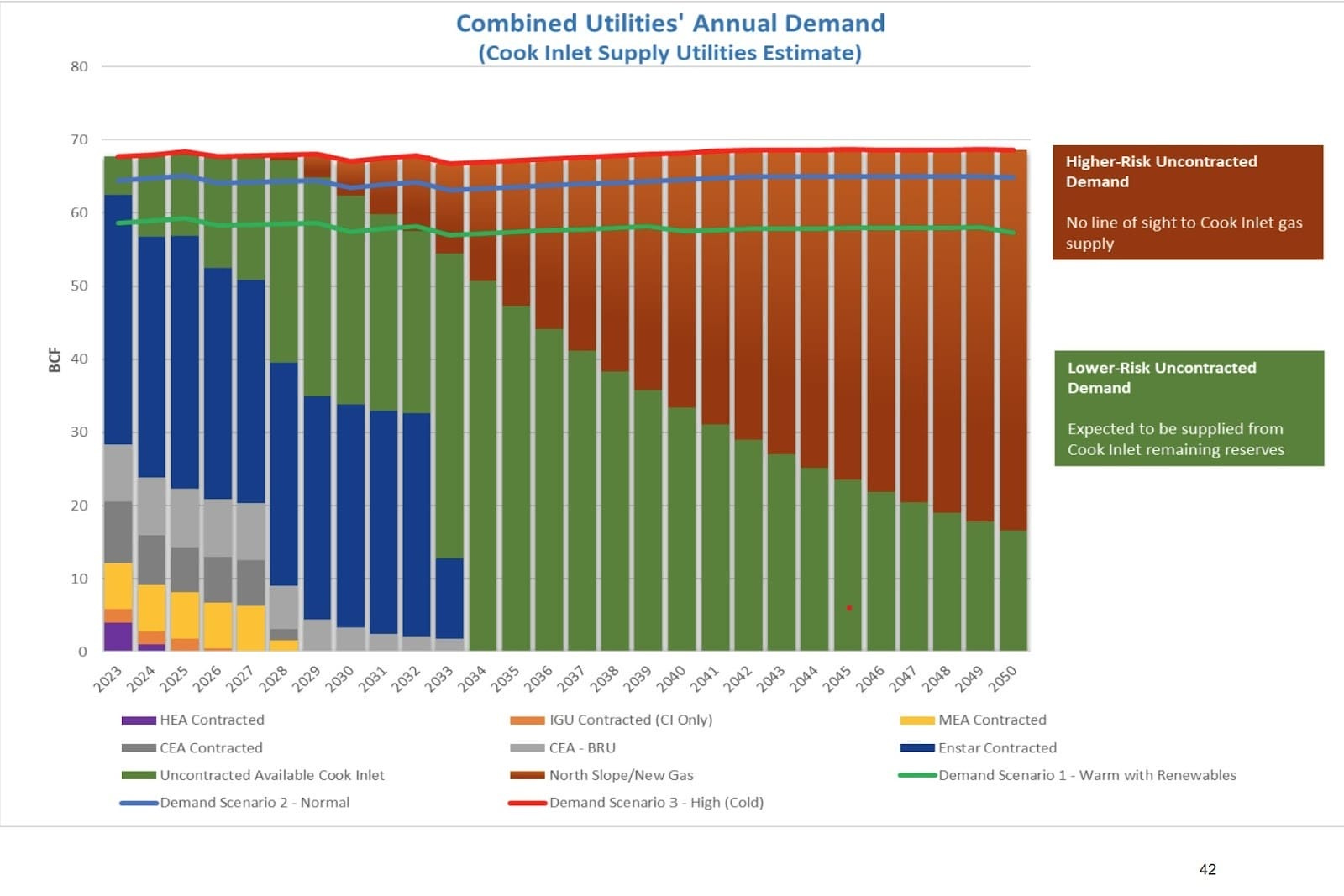

While most have heard generally of issues related to Cook Inlet gas supply, it’s helpful to understand precisely what is going on when discussing this issue. Here is a chart that Sims used during his presentation before the Committees.

The chart shows the annual supply-demand balance for the Cook Inlet by year from 2023 through 2050. The lines across the top represent the projected annual demand of Cook Inlet buyers. The red line at the very top represents projected annual demand under the “high” scenario (repeated cold temperatures). The lower, blue and green lines represent projected annual demand under the “normal” (blue) and “warm with renewables” (green) scenarios.

The colored bars below the green and red bars represent the portion of the projected demand supplied by year under current contracts between Cook Inlet producers and buyers. The green bars reflect “Lower-Risk Uncontracted Demand,” which, according to the analysis reflected in the chart, is the portion of the overall demand not currently covered under existing gas supply contracts but nevertheless “expected to be supplied from Cook Inlet remaining reserves.” The red bars reflect “Higher-Risk Uncontracted Demand,” which, according to the analysis, is the portion of the overall demand not currently covered under existing gas supply contracts and for which there is “no line of sight to Cook Inlet gas supply.”

It is clear from the chart that there are already shortfalls in meeting projected demand from currently contracted supplies under both the “normal” and “high” scenarios, with shortfalls in meeting projected demand from currently contracted supplies plus gas “expected to be supplied from Cook Inlet remaining reserves” beginning as early as 2028 under the “high” scenario and 2029 under the “normal” scenario.

The situation is not without a solution, however. There are a variety of available alternatives.

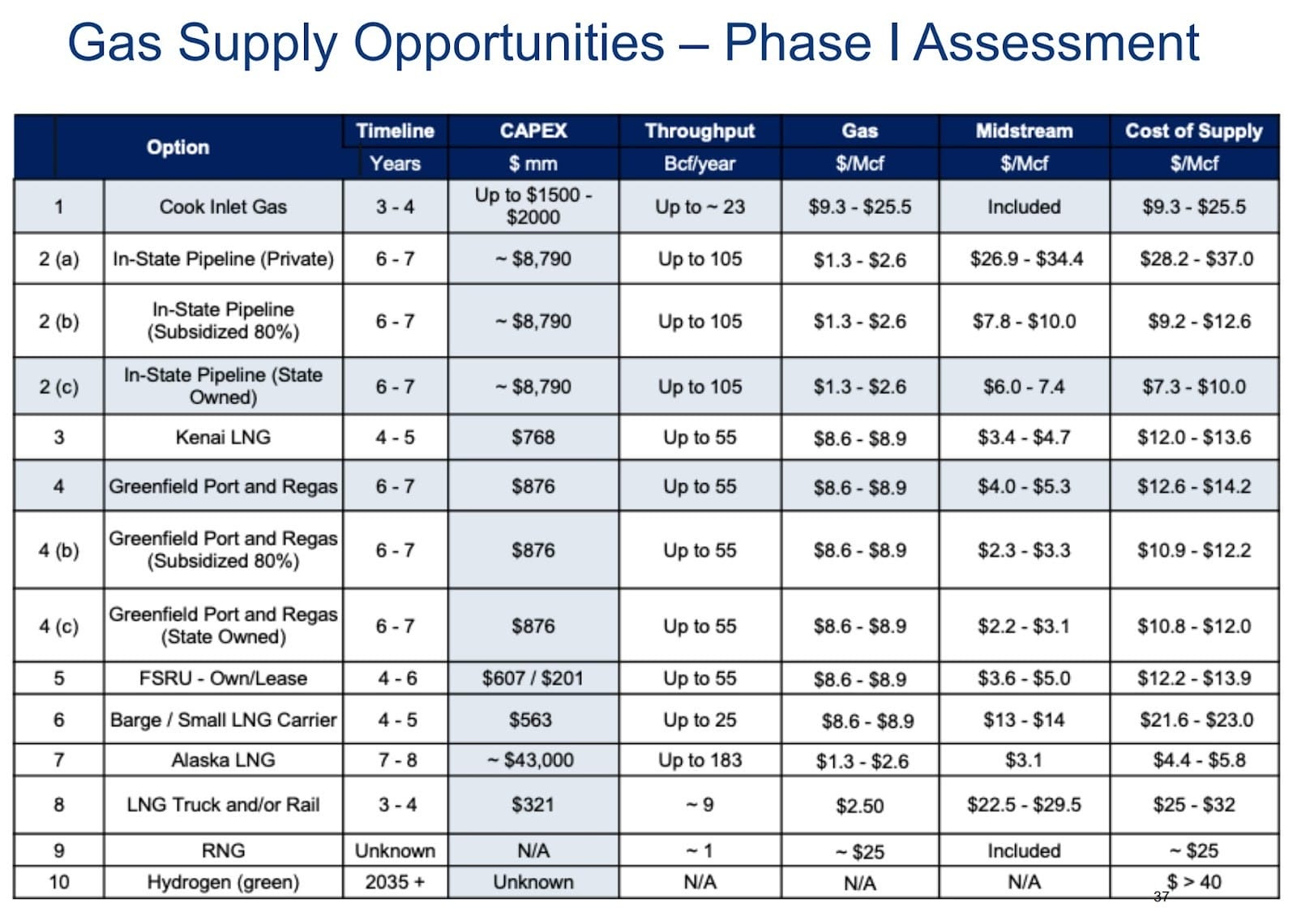

Another chart that Sims provided during his testimony looks at the potential alternatives for avoiding the shortfalls developed during Phase I of a joint study (Phase I Joint Study) published last year by the Cook Inlet utilities and others using consultants from the Berkeley Research Group (BRG) and Cornerstone Energy Services (Cornerstone).

That chart looks at the timeline for adding various new sources to the Cook Inlet gas supply, together with the projected capital cost and resulting “cost of supply” once added.

While several options involve state subsidies, either directly or indirectly (through state ownership of the facility), others don’t. Of those, three of the liquified natural gas (LNG) options – Kenai LNG, Greenfield Port and Regas, and “FSRU” (which stands for “floating storage and regasification unit”) – fit in a narrow “cost of supply” range of between roughly $12 and $14/Mcf.

On the other hand, the cost of supply from increasing Cook Inlet gas supplies beyond those “expected to be supplied from Cook Inlet remaining reserves” is projected to fall within a relatively wide band of anywhere between $9.30 and $25.50/Mcf.

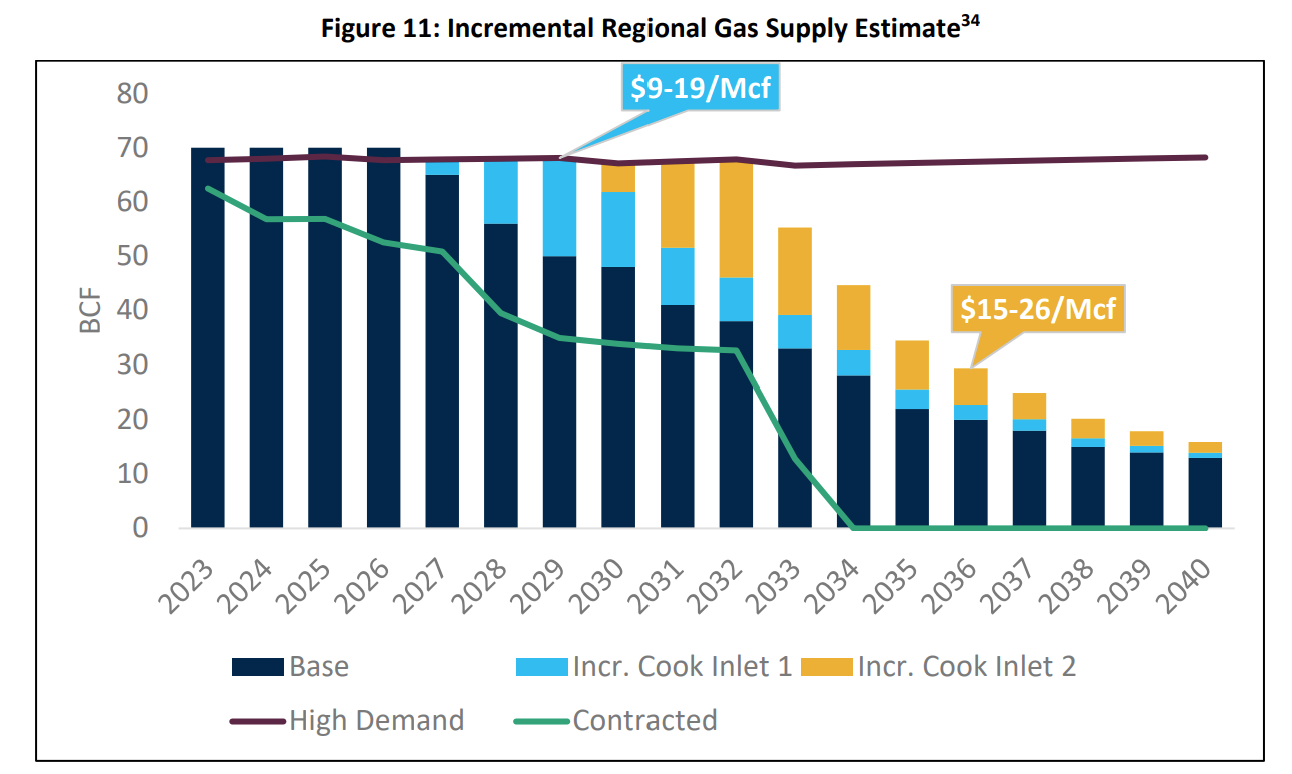

While the charts Sims provided during his testimony before the Joint Committees did not, another chart included in the Phase I Joint Study helps to explain this wide band.

That chart shows the projected incremental cost of adding Cook Inlet gas supplies sufficient to meet demand between 2027 and 2029 would be between $9 and $19/Mcf, and then between $15 and $26/Mcf to add additional supplies sufficient to meet demand three more years through 2032.

While the cost of the lower end of the first tranche of incremental supplies is lower than that of the LNG options, it quickly outstrips the cost of supply from the LNG options at the upper end of the range. Notably, the midpoint of the range is roughly 10% higher than the midpoint for the Kenai LNG option.

The cost of the second tranche of incremental supplies isn’t even competitive with the LNG options at the lower end of the range. The midpoint of the range is fully 60% above the midpoint for the Kenai LNG option.

And the analysis offers no price to add enough supplies to meet demand after 2032. Instead, looking at the entire range, the Phase I Joint Study concludes that “it is our opinion that it would be risky and unadvisable under current market conditions to count on sufficient Cook Inlet or other regional gas supply to fill the Unmet Gas Demand beyond 2026 without developing alternative supplies.”

How does that relate to whether Alaska is headed down the same road as Venezuela?

It’s simple. The level of subsidies that Alaska would need to provide to incentivize new production sufficient to meet the needs of Cook Inlet buyers is substantial. Using the midpoint of the ranges, the subsidies required to reduce the cost of the first tranche of incremental supplies just to get them down to the level of Kenai LNG would need to be in the range of $1.20/Mcf. The required subsidy level would be even greater if the goal were to reduce the cost below LNG.

And that is just to meet demand up to 2029. The numbers are much larger when looking at the second tranche of incremental supplies. Again, using the midpoint of the ranges, the subsidies would need to be in the range of $7.50 – $8.00/Mcf just to get the cost down to the level of Kenai LNG. As with the first tranche, if the goal were to reduce the cost below LNG, the required subsidy level would be much larger.

And those would simply be to incentivize sufficient production to meet demand through 2032. If additional supplies exist, the subsidies required to incentivize additional production beyond that point would be even greater.

Some argue that subsidies of Cook Inlet production are required because the cost of LNG will cause a “price shock” to consumers. That dramatically overstates the impact of LNG. Supplies delivered under existing Cook Inlet contracts will not disappear with the commencement of LNG deliveries. Just like “old” gas did in interstate markets in the early days of the Natural Gas Policy Act, the lower-priced gas that continues to be delivered under existing Cook Inlet contracts will buffer the impact of the higher-priced LNG on consumers.

Any price impact on consumers will be gradual as gas delivered under the existing, lower-priced contracts gradually declines and LNG supplies are phased in.

Others argue that waiving royalties on new production – with the resulting loss in state revenues – is not a subsidy in any event because the gas otherwise would not be produced without waiving royalties. While no one can know how the future may play out, that’s likely also not true.

Higher-priced LNG volumes will send a new, higher price signal to Cook Inlet producers. While producers may not find it economical to develop new, incremental supplies at current price levels, the economics will change when the market price for incremental supplies is reset by delivering LNG at a higher price.

At that point, producers may find it economical to develop additional supplies at the higher price. Because LNG is scalable – buyers can forego additional LNG volumes if Cook Inlet supplies are available at an equal to or lower price – they also will have a market to sell to. In that event, the state will receive royalties it otherwise would forego under the recent subsidy proposals.

We agree that there is a short-term problem that needs to be addressed. During his presentation, Enstar’s Sims said the likely date for first gas from any LNG project is now 2030. Looking at the above charts, it is clear that Cook Inlet buyers will need at least some additional supplies before that point.

But any thoughts about providing state subsidies should be tightly drawn around that window, and that window should be better defined. The problem the Cook Inlet utilities have faced this winter largely relates to deliverability – the rate at which reserves are produced. There are a number of ways of addressing that, including expansion of the capabilities of the existing Cook Inlet Natural Gas Storage facility through additional wells and, as needed, periodically tapping the ability of Matanuska Electric Association’s Eklutna generating plant to switch to fuel oil during periods of peak natural gas demand.

As we explained in a previous column, if some royalty relief is needed to incentivize the development of additional Cook Inlet supplies beyond that during that period, existing statutes already provide the Department of Natural Resources with sufficient authority to respond. Under existing AS 38.05.180(j), the DNR Commissioner “may provide for modification of royalty on individual leases” (or units) under various circumstances where the producer can demonstrate that, without the modification, production from the lease or unit “would not otherwise be economically feasible.”

The goal should be to match the scope of any relief to the short-term need. We shouldn’t allow a short-term problem to turn into long-term subsidies.

Why not? As we explained in a previous column, those subsidies would create an even bigger budget hole than Alaska already faces, likely generating even greater adverse impacts on middle- and lower-income Alaska families given the current policy of filling those holes through continued cuts in the Permanent Fund Dividend (PFD).

As happens in Venezuela, subsidies also would exacerbate the situation by artificially creating more demand than would occur if the supplies were priced at free-market levels and artificially depressing the economic case for alternative sources of supply, such as renewables, and demand-reducing options, such as increased weatherization efforts.

In short, like other markets throughout Alaska, the Cook Inlet gas market should continue to be governed mainly by free-market principles. Because reasonable alternative sources of supply are available, the consequences of doing so are not so great as to justify significant government intervention. On the other hand, the costs and distortions created by significant government intervention and subsidies may be substantial.