The Friday Alaska Landmine column: This is why and how the Permanent Fund is going to be drained

Some think the Permanent Fund principal can't be touched, but we explain why and how some are positioning to drain it once Permanent Fund Dividends are gone

Viewed from the proverbial “30,000-foot level,” Alaska’s budget history over the last twelve years has been a succession of efforts to balance a long series of deficit-ridden budgets without using taxes that would impact the top 20%, non-residents, or the oil industry.

The effort began in Fiscal Year (FY) 2013 using the Statutory Budget Reserve (SBR) to bridge the gap. Once the SBR was effectively drained, the focus turned to the Constitutional Budget Reserve (CBR). Once the end was in sight for the CBR, the effort turned to making cuts to the Permanent Fund Dividend (PFD). While PFD cuts are a form of taxation, they are a highly regressive tax approach – indeed, according to one Alaskan economist, the “most regressive tax ever proposed” – taking the largest share from middle and lower-income Alaska families.

Consistent with the goal as viewed from the 30,000-foot level, they take a trivial share of income from those in the top 20% and none from non-residents and oil companies.

The following chart follows the amounts used to plug the budget gaps over the last decade by type. In sum, over the 12-year period, the Legislature has used $27.7 billion in such measures to fill the various budget gaps, roughly $6.1 billion of which has come from the SBR, $13.5 billion from the CBR, and $8.1 billion so far from PFD cuts.

But using PFD cuts to fill the state’s continuing budget gaps won’t last forever. As we have explained in a previous column, without a significant change to its current trajectory, even the PFD likely will be gone by the mid-2030s.

What happens after that? Some who aren’t watching closely think the state will finally turn to more broad-based taxes, albeit starting with sales taxes—the second most regressive approach after PFD cuts—to continue to minimize the impact on the top 20% as much as possible. To avoid even those, others naively think the state will finally slow down its spending trajectory, matching spending to the revenue available from traditional sources plus the, by then, fully taxed PFD.

But those watching closely realize that some are already making other plans for that day by creating the ability to start draining the Permanent Fund to keep the top 20%, non-resident and oil’s “tax-free” party going long into the night.

The key to that plan is the Permanent Fund Board’s recently published Trustee Paper No. 10, which proposes to amend the Alaska Constitution to merge the two Permanent Fund accounts – the principal (sometimes called the corpus) and the earnings reserve account. Once that occurs, the Legislature can keep drawing from the Permanent Fund, even when the Fund isn’t earning enough to support the amount being drawn.

As we explained in more detail in a previous column, the Fund might survive for a time, but as with the SBR, CBR, and PFDs before it, it likely will also eventually deplete. But at a rate a bit slower than the others so that, if they play their cards right, those in the top 20% and oil will have ample time to finalize and execute their exit plans from Alaska before the Fund finally evaporates and the burden shifts back to their successors.

Here’s one potential trajectory we calculated in our previous column on this issue, looking at the impact on the Fund in real dollar (after inflation) terms at a draw rate of 5% but a real rate of return over the period of only 4%:

That column also includes other scenarios under which the Fund is drained even faster.

To help sell its plan to merge the Permanent Fund’s two accounts before the purpose becomes apparent, aided by some in the Legislature, the Permanent Fund Corporation (PFC) has rigged its accounting system to make it seem as if the earnings reserve is running out of money quickly and, thus, that a near-term merger of the two accounts is essential.

It has accomplished that through a two-step approach. As we’ve explained in a previous column, the first, undertaken by the Legislature earlier this decade, was to drain the earnings reserve account of a significant portion of its reserve by making two ad hoc $4 billion transfers from the earnings reserve account to the principal. The transfers initially were made under the guise of “prepaying” for inflation proofing, but since shortly after they were completed have been treated by the PFC instead as routine principal, with the Legislature continuing to appropriate additional annual transfers for inflation proofing as if the prepayments didn’t exist.

The effect is to charge the earnings reserve twice for the same expense: once for the “prepayment” of future inflation proofing and then again for the payment of the same “inflation proofing” as it becomes current. It should not be surprising that double charging for inflation-proofing is rapidly draining the earnings reserve account.

As we’ve also explained in another previous column, the second step in making it seem as if the earnings reserve is running out of money is for the PFC to include a significant advance accrual in its accounting for the current status of the earnings reserve account. As we explained in that column, for accounting purposes the PFC charges the current earnings reserve in any given year for the full amount of the percent of market value (POMV) draw for the following year. To make certain the account looks depleted in the run-up to the next legislative session, at the same time, the PFC includes only the portion of the projected amount of the realized earnings for the year actually received at any given point in time.

The mishmash of accruing a lump sum ahead of the curve for future expenses and following the curve for revenues accomplishes the desired effect. It makes the earnings reserve account look depleted when it’s far from that condition.

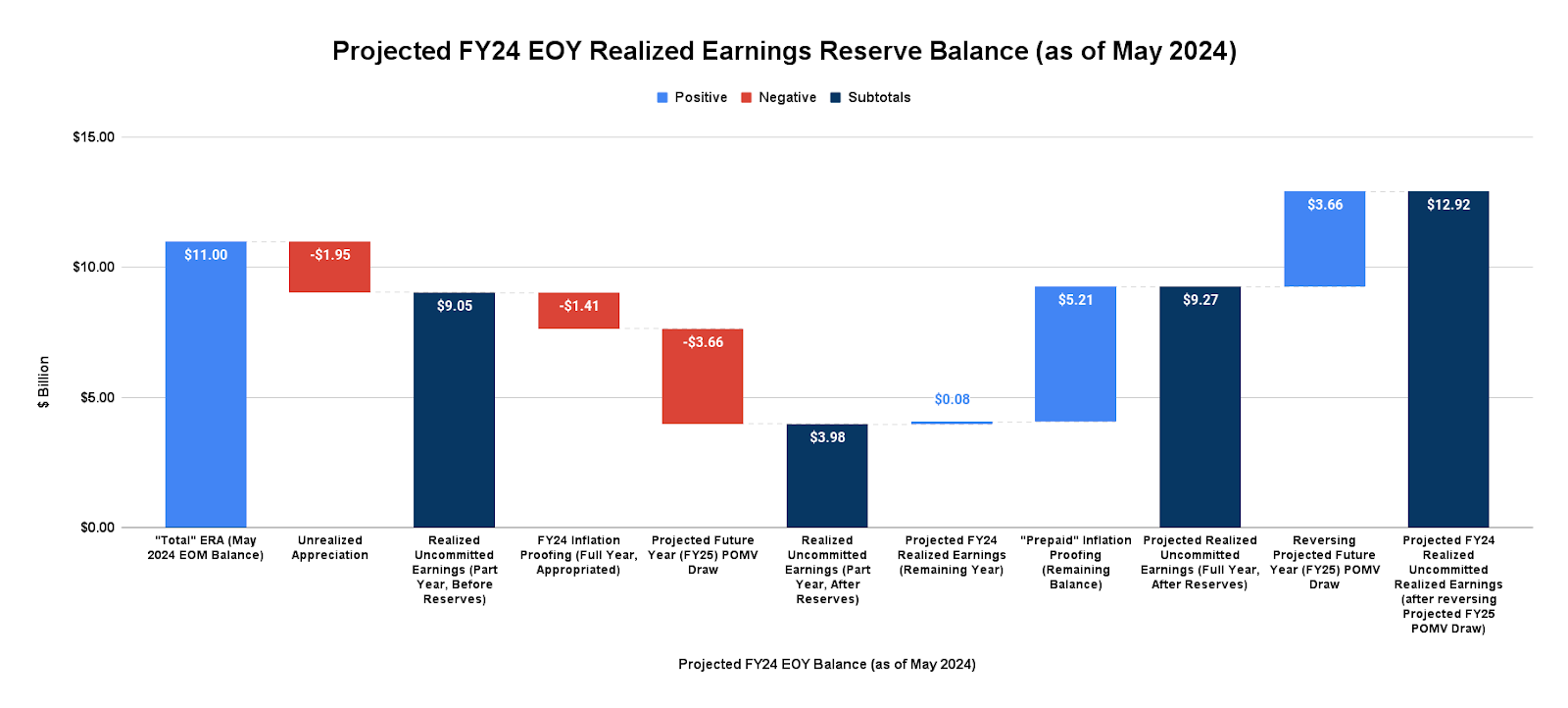

In our earlier column, we explained how to adjust for the PFC’s accounting tricks to provide a truer picture of the earnings reserve account. We have since started publishing monthly updates to the charts we developed there to show the account’s status on an ongoing basis, adjusted to eliminate the advance accrual, match the anticipated annual revenues with annual expenses, and reflect the remaining portion of the prepaid inflation proofing still embedded in the principal.

Here is our latest update based on the latest financial statements and history and projections published by the PFC. Rather than the $3.98 billion in “realized uncommitted earnings” projected in the PFC’s May 2024 financial statement, we believe the true balance of the realized uncommitted earnings held by the PFC is closer to $13 billion.

But that hasn’t stopped some of the state’s reporters from falling for the PFC’s misleading storyline “hook, line, and sinker.”

Last year, both the Alaska Beacon’s Editor-in-Chief, Andrew Kitchenman, and reporter James Brooks fell for the PFC’s line by publishing stories under the headlines “Alaska Permanent Fund account that pays for state budget, dividends is under pressure” (Kitchenman) and “New estimate shows Alaska’s Permanent Fund could be out of spendable money in 3-4 years” (Brooks).

Thus far this year, it has been Anchorage Daily News reporter Sean Maguire’s (“Permanent Fund’s spendable account faces first potential shortfall starting in July”) and Alaska Public Media reporter Eric Stone’s (“Why Permanent Fund managers are again sounding the alarm about a key account running low”) turn to fall for the PFC’s storyline, pushing the view that the accounts must be merged to avoid the Fund running out of “appropriable” (spendable) money.

But the accounts don’t need to be merged to avoid such a result. Using the remaining prepayments, the Legislature can go nearly 3.5 years at projected inflation levels before making additional transfers from the earnings reserve account to the principal for inflation-proofing. Retaining that money in the earnings reserve account instead will significantly extend its life. The same is true from an accounting perspective by moving the charge for the POMV transfer from the year before it is due to the year it is due.

As the most recent projections included in our monthly update show, even at the subpar (below CPI +5%) income levels the PFC currently projects over the next decade, those steps alone will extend the life of the earnings reserve account (the blue bar in the chart below) at healthy levels well beyond FY33. There is no immediate crisis.

Over the longer term, some argue that limiting draws to 5%, as proposed in the most recent House version of the PFC’s proposed Constitutional Amendment, or 5.5%, as proposed in the Senate counterpart, will protect the Fund against the potential for overdraws.

But that’s also not true. That argument assumes that the Permanent Fund regularly replenishes the Fund by earning at least the same amount that’s being drawn out on an ongoing basis. However, as the charts in one of our columns last month show, the Permanent Fund went through a long period in the late 2000s and early 2010s when it failed to earn the requisite CPI +5% (much less 5.5%). The charts show that the Permanent Fund is also going through the same shortfall currently. And by failing to cover the POMV draw plus inflation proofing, the PFC’s own earnings projections appear to show that it fails to continue to do so in the decade ahead.

Failing that, the Permanent Fund will gradually decline at a 5% or 5.5% draw, at least on a real (after inflation) basis, if not from a nominal perspective.

The incentives also change in the years ahead once the PFD is drained. The PFD is the current generation of Alaskans’ only real attachment to the Fund’s health. Realistically, Alaskans care about the Fund only to the extent they are focused on its ability to produce healthy PFDs.

Consequently, once the PFDs are gone, the incentives will change dramatically. Beyond that point, the then-current generation of Alaskans will care about the Fund only to the extent that it can be used to shield them from paying taxes. If overdraws are necessary to do that, so be it. Because PFDs are no longer being distributed, then-current Alaskans won’t worry about the impact of a falling Fund on those. The incentives will be entirely focused on avoiding taxes.

Some claim Alaskans won’t be so “short-sighted,” but the recent experience with the SBR, CBR, and PFD clearly proves otherwise. Because the current generation of Alaskans realized no benefits from the SBR and CBR, they only cared about using it to avoid taxes. As a consequence, we have seen those reserves drained by nearly $20 billion within the span of only a little over a decade.

While middle and lower-income Alaskan families care about PFD levels, the top 20%, non-resident industries, and oil companies don’t. Using their political power, they’ve been able increasingly to divert the PFD from its intended purpose instead to using it to shield them from taxes until it is also well on the way to being fully depleted.

It’s easy to imagine that the same thing will happen to a single, fully accessible Permanent Fund account once PFD cuts are no longer sufficient to shield the top 20%, non-residents, and oil from taxes.

In short, some in the top 20%, non-resident industries, and the oil companies are already thinking ahead to the point at which the PFD is depleted and no longer available to shield them from paying taxes to fund the size of government Alaskans have built. Using a manufactured “emergency” as a cover story, they are proposing to take steps now to change the incentives and structure in a way that will enable them at that point to tap into the Permanent Fund principal to continue to fund their tax-free party well into the years ahead.

As we explained in our column two weeks ago, to stop it, Alaskans concerned about the state’s fiscal future should strongly urge the Governor and Legislature to take the steps necessary to restructure the Permanent Fund Board that, among other things, has published Trustees Paper No. 10, reset the draw rate to one that better reflects the Fund’s actual returns, and postpone if not outright reject, the Permanent Fund Board’s proposal to merge the two existing Permanent Fund accounts into a single, depletable one.

Otherwise, as the aptly named cartoon character Porky Pig would say, the Permanent Fund is clearly on the path to “Th-Th-Tha, Th-Th-Tha, Th-Th… That’s all, folks!”

BK like a holy irritatant in the wounded economic (Legislature’s) side. Truth to power Brad, truth to power.