The Friday Alaska Landmine column: Dunleavy to potential investors and others: 🤷♂️

By completely ignoring one of his most important fiscal responsibilities, Governor Dunleavy is failing to provide needed economic leadership, creating significant uncertainty for investors and others

Although not widely understood, complying with AS 37.07.020(b)(2) is one of the Alaska governor’s most important fiscal responsibilities. As part of the statutorily required responsibilities related to the annual budget submission, subsection (b)(2) provides as follows:

(b) In addition to the budget and bills submitted under (a) of this section… [t]he governor shall also submit a fiscal plan with estimates of significant sources and uses of funds for the succeeding 10 fiscal years. The fiscal plan

…

(2) must balance sources and uses of funds held while providing for essential state services and protecting the economic stability of the state …

The statutory obligation is among the most important because it is the only time the state’s fiscal condition is examined comprehensively over an extended period. While the Legislative Finance Division (LFD) also provides similar projections before and during each legislative session, it relies on the administration’s revenue projections.

The governor is the only person with insight into both the revenue and spending outlooks.

An extended, comprehensive forward look is important because it provides an early warning system for the state’s economic stability. At this point in the state’s fiscal history, running extended, unanticipated deficits would put the state in an extremely difficult situation. Because the state has already largely drained accessible savings, it would need to rapidly cut spending, increase taxes, issue debt, or employ a combination of all three. Unplanned spending cuts would eliminate programs on which various constituencies rely, increasing taxes would drain additional resources from the state’s private sector and families, and issuing debt would increase current and future costs.

If undertaken without adequate thought and planning, any of the three could seriously disrupt the state’s ongoing economic stability.

The purpose of the “(b)(2)” plan is to provide significant notice of the potential for such a development so that there is adequate time to analyze the alternatives and prepare a well-thought-out response. This includes giving those likely to be affected by the response—such as current and potential investors in the state—time to prepare well-thought-out responses of their own.

As an integral part of the comprehensive outlook, the governor is also charged under the statute with developing a plan to “balance sources and uses of funds … while providing for essential state services and protecting the economic stability of the state.” In short, proposing a response if the outlook is negative over the period.

That is equally as important a responsibility as providing the raw data. As explained in last Sunday’s Alaska Landmine “Sunday Minefield” by Neil Steininger, the “budget correspondent” for the Alaska Political Report and a former director of the Governor’s Office of Management and Budget, “[b]ecause the Legislature is made up of 60 members with diverse and nuanced views, it is extremely challenging for them as a body to introduce and champion major structural changes without the support and lead of the executive branch.”

Moreover, because Governor Mike Dunleavy (R – Alaska) is in charge of the Department of Revenue, between the two bodies, he alone has the information and resources needed to develop a thoughtful and low-impact revenue plan. As full-time officials – compared to the part-time Legislature – the Governor and others in the administration also have more time and resources to devote to the effort.

It is also important to provide a plan early in the budget cycle. Depending on the size and nature of the deficits, the proposed response may require significant legislative analysis and work. Requiring that the governor submit a plan for dealing with any projected deficits with the other budget components by December 15, roughly a month before the beginning of the legislative session, provides the Legislature with needed additional time to absorb and consider the proposed plan and alternatives.

Measured against these obligations and responsibilities, Governor Dunleavy’s FY2026 “(b)(2)” plan is nearly a complete failure, bordering on – if not crossing the line into – neglect and nonfeasance of his duties.

The FY2026 submission by the Dunleavy administration mostly satisfies the initial subsection “b” requirement to include “estimates of significant sources and uses of funds for the succeeding 10 fiscal years.”

The submission completely fails, however, to meet the subsection (b)(2) requirement that it additionally includes a plan that “balance[s] sources and uses of funds held while providing for essential state services and protecting the economic stability of the state.”

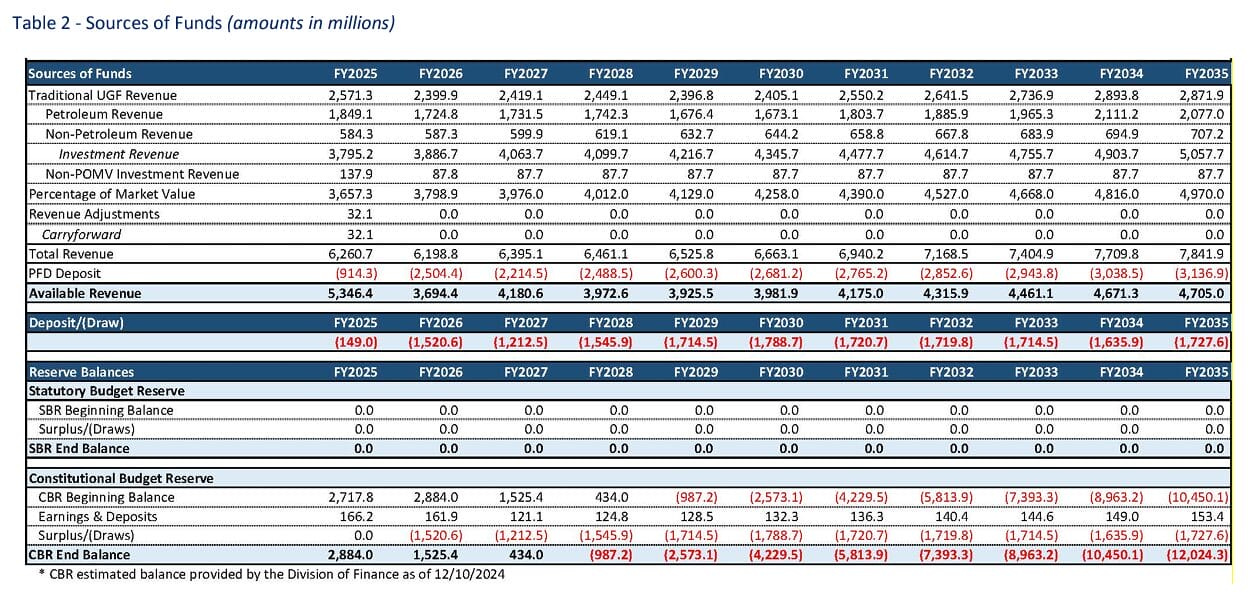

Here are the summary charts from the Governor’s submission:

Consistent with the initial requirements of subsection (b), the first chart shows “estimates of significant .. uses of funds for the succeeding 10 fiscal years;” the top half of the second chart shows the same for sources. Halfway down the second chart, the net of the two is shown under the heading “Deposit/Draw.” It clearly shows fiscal deficits in red throughout the period.

Consistent with the “(b)(2)” obligation, the bottom half of the second chart should reflect the Governor’s plan for balancing the sources and uses of funds over the period.

However, it only compares the deficits to the state’s two accessible savings accounts, the “Statutory Budget Reserve” and the “Constitutional Budget Reserve” (CBR). The result shows the balance of the state’s tertiary savings account, the CBR, after deducting annual budget deficits. While the CBR contains sufficient funds to cover the annual deficits through FY2027, it is exhausted at that point and starts running what appears to be worthless IOUs after that.

Contrary to the statutory requirement of “must,” beyond FY2027, neither the charts nor the text of the Governor’s submission “balance sources and uses of funds held while providing for essential state services and protecting the economic stability of the state.”

All that the chart shows is a giant, gaping, and ever-growing fiscal hole. And all that the text of the Governor’s submission says on the subject is this:

Alaska faces some tough fiscal challenges ahead. Policy makers continue to grapple with the current structure of the State budget, with solutions to revenue shortfalls, the ongoing discussion year after year. From new revenue measures to budget reductions, to changes to the permanent fund dividend program, the solution is not simple nor is it easily agreed upon.

Both the chart and the text are the rhetorical equivalent of a giant shrug. They certainly are not a “fiscal plan [which] balance[s] sources and uses of funds held while providing for essential state services and protecting the economic stability of the state.”

In response, the Governor cannot claim as an excuse that there aren’t available options to present.

For example, as we will discuss in greater detail in future columns, a significant part of the problem facing the state is obvious from the Fall 2024 Revenue Sources Book (Fall 2024 RSB) issued by the Department of Revenue at the same time as the Governor presented his budget. Piecing together production and revenue data, the Fall 2024 RSB clearly shows that while oil production is growing by over 42% over the period and gross revenues from that production (at projected ANS West Coast price levels) by over 20%, state revenues from production tax and royalty, the two revenue sources most closely tied to that production, are dropping over the same period by over 23%.

In other words, while the gross revenues received by the producers are projected to increase over the period, the share of those revenues received by the state is projected to drop from nearly 15% in FY2024 to a little over 9% by FY2034.

State revenues would be nearly $500 million higher if total production tax and royalty remained at FY 2024 levels. They would be nearly $930 million higher if they grew at the same rate as gross revenues. For perspective, if they grew at the same rate as production, state revenues would be nearly $1.4 billion higher or within 13% of the projected FY2034 deficit.

While it may be too much to propose that state revenues climb at the same rate as production levels, in the current context, we don’t think it’s unreasonable to expect, as part of its 10-year plan, that the Dunleavy administration proposes the adjustments necessary to hold state revenues at least at FY2024 levels over the period if not grow them at the same rate as gross revenues. Indeed, as we have explained in previous columns, we think the administration and Legislature are leaving money on the table in violation of the Constitution if they don’t.

Other revenue options are also readily apparent. For example, the ultra-broad sales tax introduced in the last Legislature (HB 142), which we analyzed in depth in a previous column, is already teed up with legislative language. By eliminating the companion reduction to the corporate income tax, the amount raised through the HB 142 sales tax alone would be sufficient to close the deficits projected in the Governor’s 10-year plan.

Alternatively, the Governor could propose an approach equivalent to the one recommended in the Final Report of the Legislature’s 2021 Fiscal Policy Working Group. That approach consisted of an “all of the above” mix of some spending cuts, some reductions in the Permanent Fund Dividend (PFD), some new revenues, and some spending limits, which would broadly spread and, through that, minimize the burden of the response on any one group.

But the Governor has chosen none of those options or any other alternatives in the FY2026 10-year plan. Instead, in violation of the statute and dereliction of his responsibilities, he has proposed nothing to “balance sources and uses of funds held while providing for essential state services and protecting the economic stability of the state.”

As we said earlier, AS 37.07.020(b)(2) establishes one of the Alaska governor’s most important fiscal responsibilities. It isn’t a mere ministerial task; it is a substantive responsibility that produces a plan vital to legislators, those in and adjacent to the public sector reliant on state spending and service levels, those in the private sector concerned about the levels at which and how the state may raise needed revenues, and others concerned with both the near and long-term economic stability of the state.

That includes potential investors and others who might be interested in relocating to the state. Who would make a significant investment or move to a state facing massive deficits that doesn’t have even the barest outline of a plan for dealing with them? Even those doing the most elementary due diligence will be concerned about the uncertainty over the levels at which they might later be required to contribute toward resolving the deficits after sinking the costs involved in making the move.

But rather than fulfilling his responsibility to the state and others affected by it, Governor Dunleavy has given the equivalent of a shrug. This dereliction of duty should not be tolerated.