The Friday Alaska Landmine column: Why the Permanent Fund earnings reserve account is not in danger of being drained

Some claim that, without merging the Permanent Fund's current two accounts into a single account, the Fund's earnings reserve account could fail. We explain why that concern is badly misplaced.

In last week’s column, we explored an issue underlying the arguments of some who are proposing to amend the constitutional provisions governing the Permanent Fund. The proposed amendment would change the Permanent Fund structure from a two-account to a one-account approach.

Under Article 9, Section 15 of the Alaska Constitution, the Fund is divided into two accounts: the principal and “income from the permanent fund.” The principal is constitutionally protected. It “shall be used only for those income-producing investments specifically designated by law as eligible for permanent fund investments.” It cannot be used for any other purpose.

Only “income from the permanent fund,” most, but not all of which is held in a second account - the statutory earnings reserve account - can be used to cover statutory distributions and other general fund spending.

Those pushing to amend the structure propose to merge the two accounts. While the proposal purports to limit the overall amount that could be drawn from the resulting single account, the portions currently held as principal would no longer be constitutionally protected. Instead, amounts which, under the current constitutional provisions, would be protected, could be drawn down to cover statutory distributions and other general fund spending.

For the reasons we explained in detail in last week’s and other, previous columns, we and others strongly oppose the proposed merger.

One of the arguments used by those pushing the proposal is that, under the current two-account structure, the funds in the earnings reserve account could be drawn down to the point that they no longer would be sufficient to meet the statutory percent-of-market-value (POMV) draw used to cover Permanent Fund Dividends (PFD) and provide supplemental support to general fund spending. In testimony this past session, the Legislature’s Legislative Finance Division (LFD) claimed that there was a 50% likelihood of such a failure.

But such a claim is based on using the cash maintained in the earnings reserve account to cover both the POMV draw and the so-called “inflation proofing” of the corpus required by AS 37.13.145(c). LFD’s testimony drops the likelihood to below 20% if the cash is used only to cover the POMV draw.

As we explained in last week’s column, the “income from the permanent fund” (to use the phrase from the Constitution) comes in two parts. One is cash or cash equivalents. The second is in what former Permanent Fund Corporation (PFC) CEO Angela Rodell has referred to as “unrealized gains – paper increases in asset values.” While both constitute income under generally accepted accounting principles (GAAP), only the cash or cash equivalents are deposited into the earnings reserve account. For internal purposes, the PFC assigns the portion of the “income from the permanent fund” accounted for as “unrealized gains” to both the first account and the second.

As we also explained in last week’s column, only the POMV draw is required to be paid in cash. The POMV draw requires cash because it is used either to fund PFD distributions or to help pay for government spending. Both PFD recipients and government vendors are paid cash.

On the other hand, “inflation proofing” is a non-cash requirement. The purpose is to ensure that the overall value of the principal is adjusted to keep pace with inflation. That is as easily achieved with appreciated assets as it is with cash.

In last week’s column, we looked at the historical levels of cash and non-cash income and balanced those against the cash (POMV) and non-cash (inflation-proofing) requirements. We found that, viewed from a historical perspective, the cash earnings were more than sufficient to cover the cash requirements and that, while a bit short over the extended periods we analyzed, the non-cash income met most of the non-cash requirements. We also found that the cash remaining after meeting the cash requirements was more than adequate to offset the non-cash income shortfall.

In short, we found that the earnings reserve balances never ran short - or even low - over an extended period if all of the “income from the permanent fund” (both cash and non-cash) was used to meet the respective uses to which the income could be put.

Using that as a base, the purpose of this column is to look at the issue going forward. In doing so, we use the history and projections of cash and non-cash income, and cash and non-cash requirements, reflected in the PFC’s most recent “Fund Financial History & Projections” report (as of April 30, 2025).

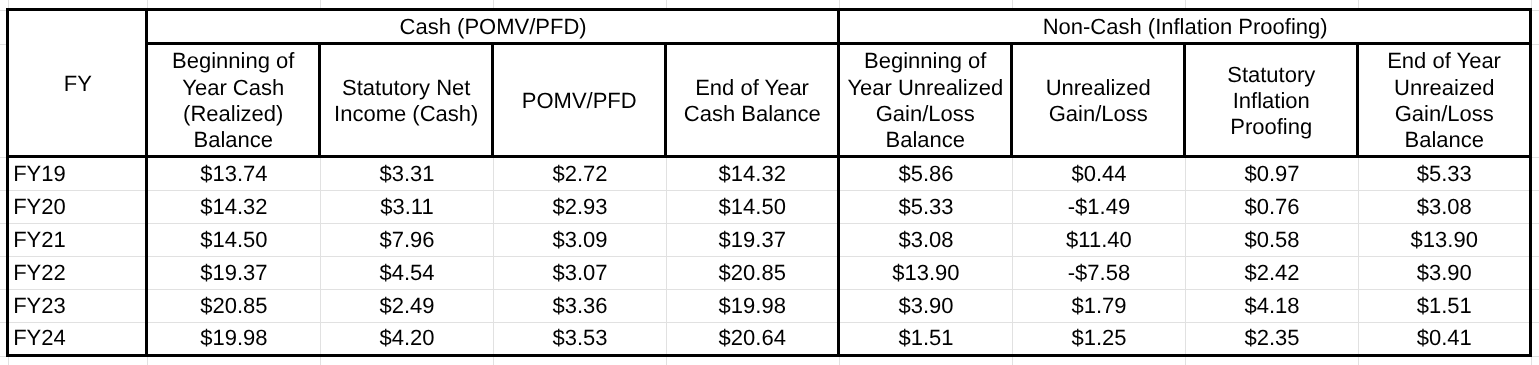

Here is the experience to date from the start of the POMV draws, restated to apply the cash income to the POMV draw and non-cash income to statutory inflation proofing. As of the beginning of Fiscal Year (FY) 2019, the earnings reserve (cash) account had a balance of $13.74 billion. The balance of the income from the Fund, accounted for at the time as accumulated unrealized gains/losses, was $5.86 billion.

The left side of the chart reflects the changes to the cash balance going forward from income realized as cash (so-called “statutory net income”) and draws made for the POMV. The right side of the chart reflects the changes to the non-cash balance going forward from income accounted for as unrealized gain/loss and draws for statutory inflation proofing.

As the chart demonstrates, over the period, the balance of statutory net income (cash) grew from $13.74 billion at the start to $20.64 billion at the end. Annually, incoming cash (statutory net income) exceeded outgoing cash (the POMV draw) in every year except one (FY23). The accumulated balance was more than enough to absorb the excess draw for that year.

While the non-cash balance declined from $5.86 billion at the start to $410 million at the end, the balance was still positive. The non-cash side didn’t require any supplements from the cash side to meet the inflation-proofing requirement.

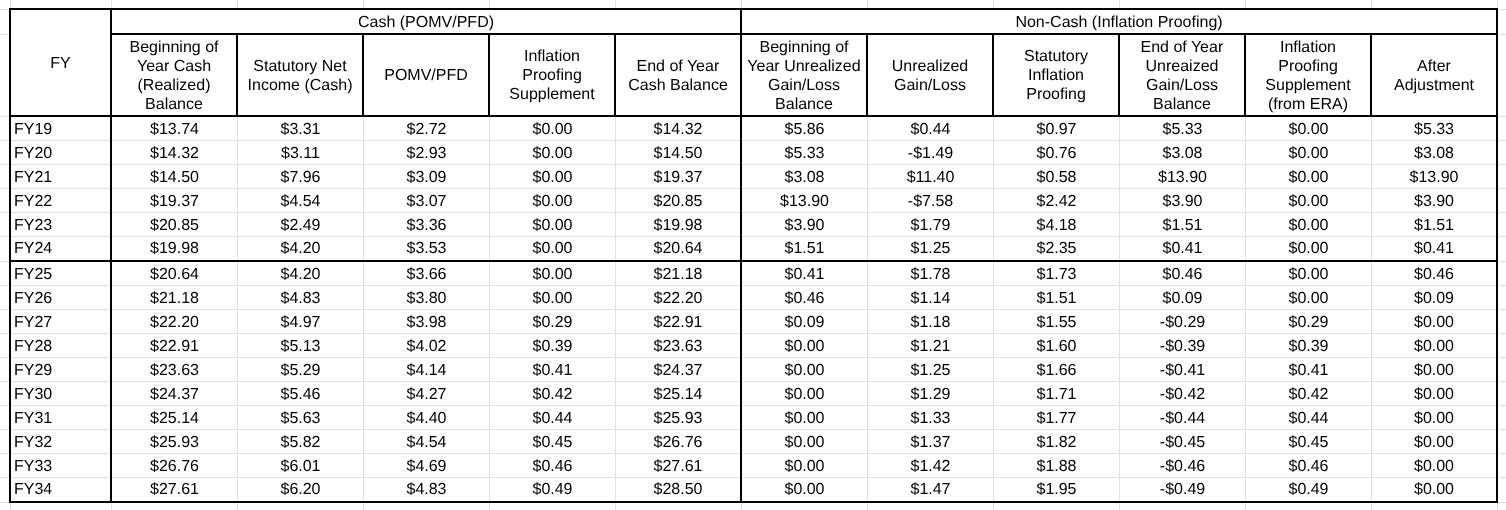

This chart extends those numbers going forward for the period covered by the PFC’s most recent “History & Projections” report:

Over the extended period, the cash balance continues to grow, from a balance of $20.64 billion at the start of FY25 to $28.50 billion at the end of FY34. Even with an additional use, incoming cash exceeds outgoing cash every year.

The additional use is to supplement the inflation-proofing requirement. As the right side of the chart shows, beginning in FY27, the amount required annually to cover the inflation-proofing requirement is more than the projected balance of unrealized gain/loss. To compensate for that, the chart projects setting aside a portion of the accumulating cash to supplement the inflation-proofing requirement beginning in FY27.

But as the chart also shows, the cash required for that purpose is only a portion of the inflation-proofing requirement, and is well within the bounds of the excess statutory net income (cash) being generated over the period. In total, from FY25 through FY34, the permanent fund is projected to generate over $53.5 billion in cash income. Of that, it is projected only to use $42.3 billion to cover the POMV draws, leaving a positive $11.2 billion for the period.

The amount projected to be required to supplement the inflation-proofing requirement is only $3.34 billion, less than a third of the remaining cash balance. Even accounting for that, the projected balance over the period is still a positive $7.86 billion.

Including the previous balance accumulated during the entire period from FY19 through FY34, the balance of the earnings reserve account never drops below $20 billion. It ends the period with a balance of $28.5 billion. Both are far from the point of exhaustion.

In short, the balance of the earnings reserve account runs low only by excluding the portion of the “income from the permanent fund” classified as “unrealized gain/loss.” However, while not realized as cash, under GAAP, that is also “income from the permanent fund,” and thus available to meet statutory obligations. Once applied to the non-cash requirements, it is clear that the remaining balance of the “income from the permanent fund” held in the earnings reserve account is not only positive but also robust.

The concerns about potentially “draining” the earnings reserve are greatly overstated and result only from completely disregarding a significant source of “income from the permanent fund” that could be used to meet the inflation-proofing requirement. Once adjusted to account for the additional source, the concerns dissipate.

For those interested, we have also published a supplement to this column at https://bgkeithley.substack.com/p/supplement-to-may-23-2025-alaska.