The Friday column: "Process"

Some claim the S-corp tax should be rejected because it hasn't undergone a legislative "process." This week, we compare its review to the "process" used to determine Alaska's largest tax.

A comment from a listener during our segment on the Michael Dukes Show earlier this week made us stop and think. In response to a question from Michael, we explained that the Alaska Senate’s recent focus on closing the S-corp tax loophole (and, through that, also a focus of the Legislature’s Conference Committee on HB 381) shouldn’t come as a surprise, because the issue has been percolating since 2019, when BP announced that Hilcorp would be acquiring BP Alaska’s interests.

While BP had been paying Alaska’s petroleum corporate income tax up to that point, Hilcorp would not, because it was formed as a so-called “S-corporation” (a reference to a subchapter of the federal corporate income tax code), which enabled it to slip through a crack in Alaska’s somewhat dated petroleum corporate income tax code. Various legislators and commentators, including us, have been discussing the importance of closing the so-called “S-corp loophole” since then.

In response, the listener argued that, while it may have been the subject of discussion, closing the loophole had not received adequate legislative scrutiny. While there had been bills filed addressing the issue, the listener argued that the work needed to vet them fully hadn’t been completed, or, using his words, the bills had “never made it through the process.”

That made us think about the “process” that has been followed in setting what, for eight of the last ten years, has been Alaska’s biggest tax. The answer is that there has been virtually none.

Some think Alaska’s biggest tax is the state’s oil production tax. But, in fact, it is a far distant second.

Over the past decade, the biggest, by far, has been the withholding and diversion to government of (i.e., tax on) Permanent Fund Dividends (PFD), what Professor Matthew Berman of the University of Alaska - Anchorage’s Institute of Social and Economic Research (ISER) has called the “most regressive tax ever proposed.”

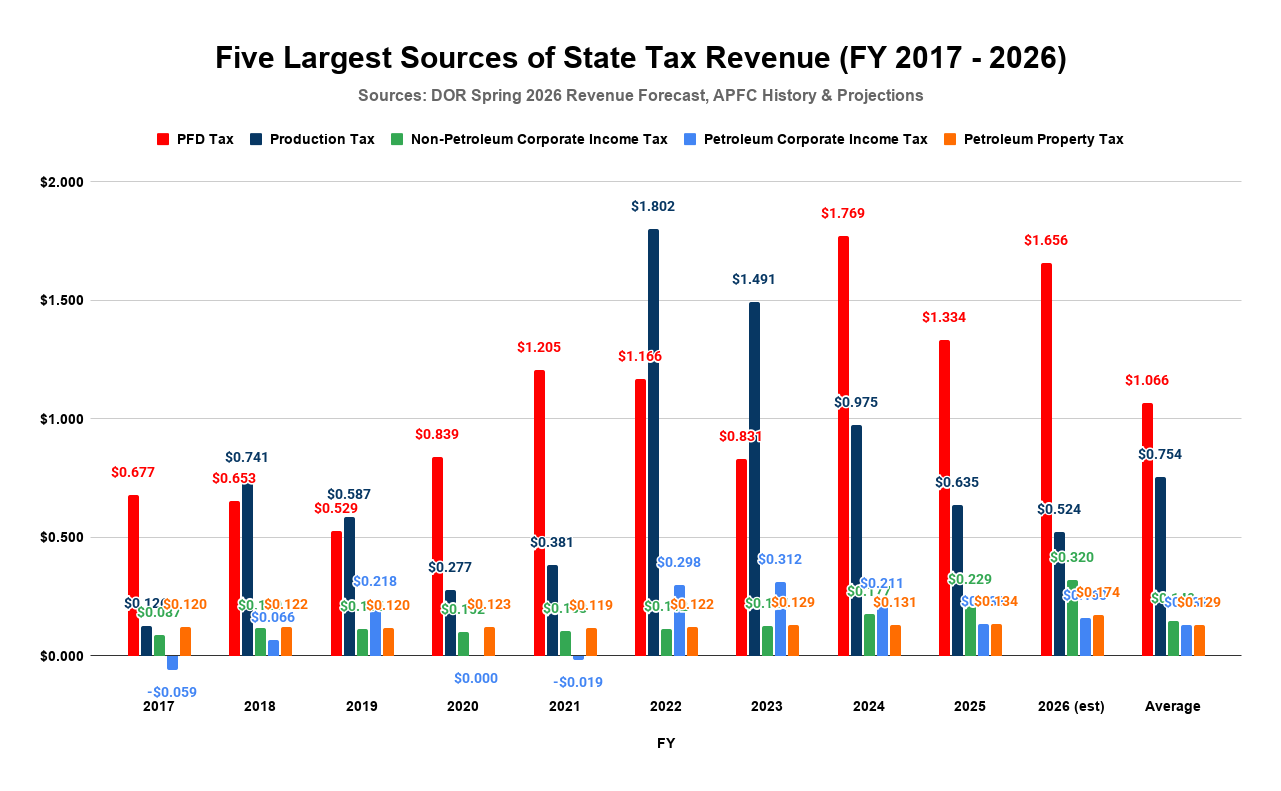

Here is how the two largest sources of tax revenue, along with the other top five sources, compare over the last ten years.

On average over the period, the state’s PFD tax has produced $1.066 billion in revenue annually.

By comparison, the state’s production tax has produced only $754 million per year in revenue. The other three of the state’s top five taxes, the state’s non-petroleum corporate income tax, the petroleum corporate income tax, and the petroleum property tax, respectively, have produced only $149 million, $132 million, and $129 million per year each. In sum, the other four sources combined have produced only about as much as the PFD tax alone has.

The S-corp tax is projected by the Department of Revenue (DOR) to raise only $100-$200 million per year during its first 10 years. Even at its peak, around 25 years out, it is only projected to raise a little over $600 million per year, far short of what the PFD tax has produced over the past 10 years.

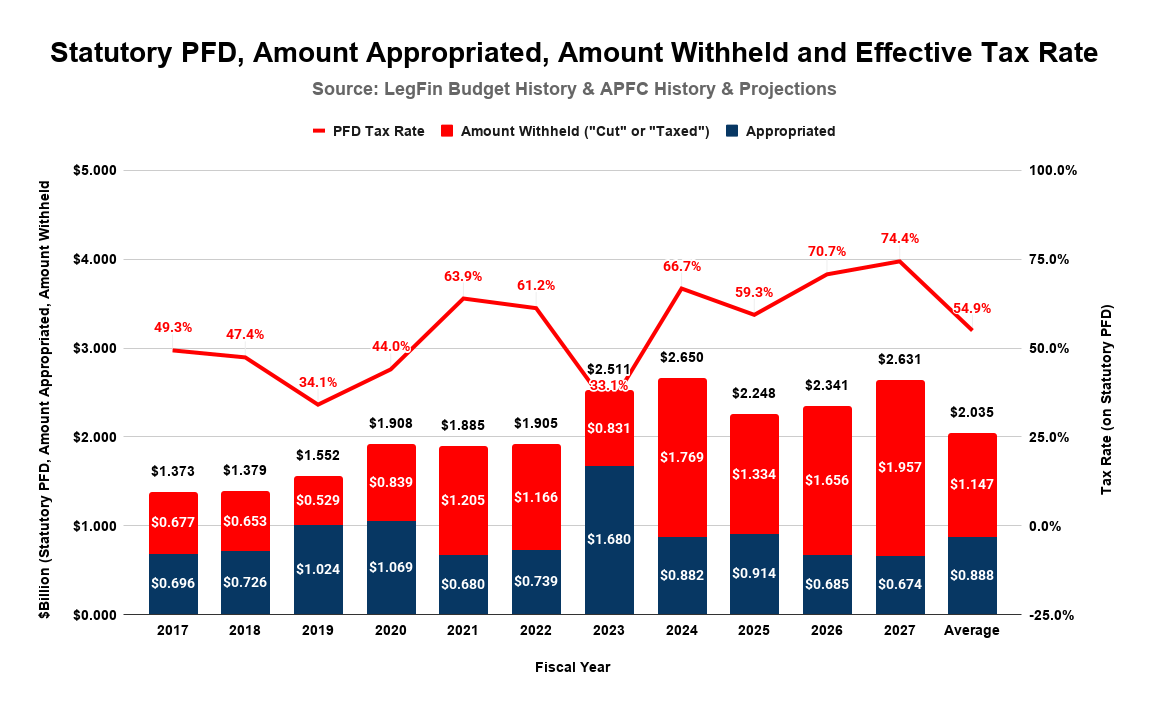

While some have argued that engaging in a “process” on the S-corp tax is important because it could affect the Alaska LNG project, the PFD tax is equally (if not more) significant for Alaska households. Here is the tax amount as a share of the statutory PFD per year since its first application in Fiscal Year (FY) 2017.

On average over the period, nearly 55% of the PFD has been withheld and diverted to the government annually. In sum, the amount withheld from Alaska households over the period totals over $12.5 billion.

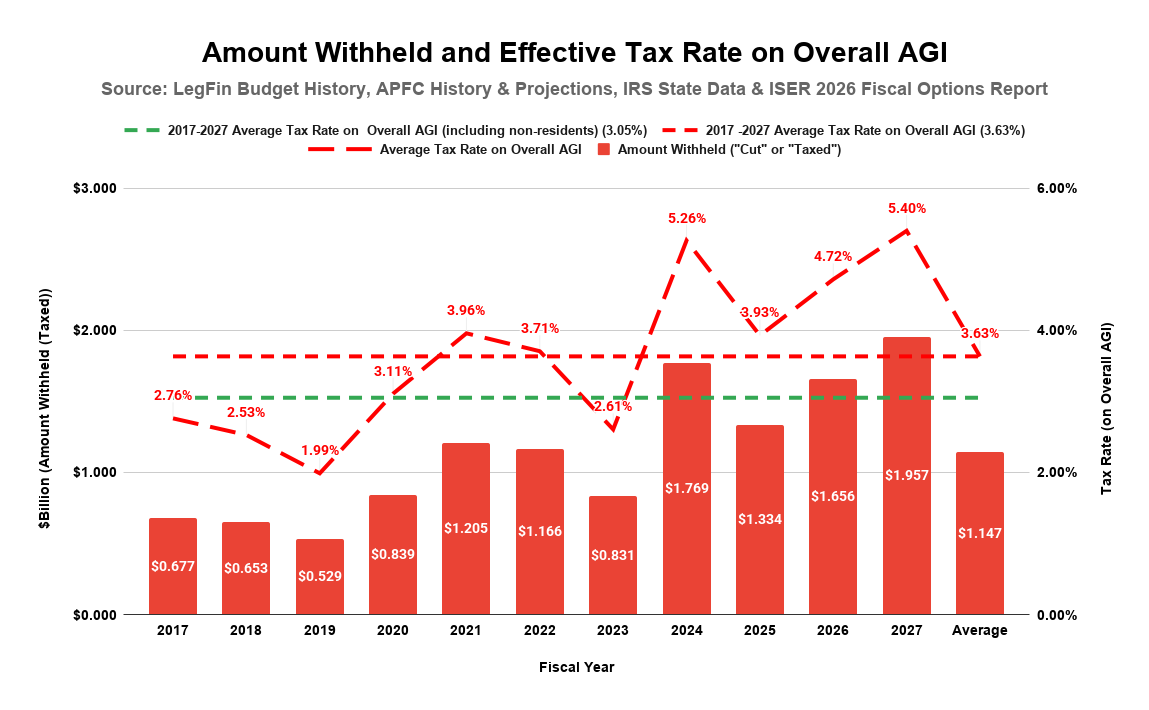

This represents a significant share of Alaskan household income over the period. Using as a base Alaska Adjusted Gross Income (AGI) as reported by the Internal Revenue Service (IRS) through federal tax year 2022 (the latest year currently available) and increasing it thereafter by inflation, here is the share of Alaska AGI withheld and diverted (i.e., the effective tax rate) by year through the PFD tax.

While the effective tax rate on AGI over the entire period (the dashed red line) averages 3.63%, over the last four years it has averaged 4.59% of Alaska AGI.

Yet, in all of the time the tax has been in effect, we don’t recall any of those personal taxes being subject to the same type of extensive legislative “process” that the listener argued should be applied to the S-corp fix.

The Legislature didn’t even review the first PFD tax. Instead, then-Governor Bill Walker (I-Alaska) created it by line-item vetoing its legislative appropriation. To protect his members from going on the record on whether to override the veto, then-Senate President Sen. Kevin Myers (R-Anchorage) refused even to call the veto up for an override vote.

Notwithstanding being repeatedly reminded over the years that, of the alternatives, using PFD taxes has the “largest adverse impact on the [overall Alaska] economy” and on middle and lower-income Alaska families, subsequent legislatures have continued the practice by appropriating PFD levels at amounts significantly less than the statutory amount, without assessing the impact of the reductions on the fiscal health of Alaska households and the Alaska economy, or comparing those effects to alternatives.

Indeed, to our knowledge, despite the significance of the issues, there haven’t even been any hearings on the role PFD taxes play in worsening the state’s outmigration problem or in increasing the cost to the state of various safety-net programs, which are a significant driver of rising state spending. Using PFD taxes reduces the income of working-age middle- and lower-income Alaska families - the core of the state’s outmigration problems - more than either sales or income taxes would. Replacing PFD taxes with lower-impact alternatives would increase income for working-age middle- and lower-income families, reducing their incentive to migrate to other states.

Because of their greater impact on lower-middle- and lower-income Alaska households, PFD taxes also increase the state’s poverty levels more than alternative taxes would. That, in turn, drives up the cost of the state’s various social safety-net programs. Substituting alternatives for PFD taxes would reduce poverty and near-poverty levels, reducing the costs of the state’s safety net programs.

Moreover, to our knowledge, the Legislature has not taken the time to assess the overall impact on the fiscal health of Alaska households and the Alaska economy when voting for significant increases in the annual tax rate. The Legislature has voted to increase the effective tax rate over the prior year in four of the last five years, more than doubling it over that period from 2.61% of Alaska AGI in FY2023 to 5.40% in FY2027. Yet, there has been no “process” to vet the impact of such significant increases on the fiscal health of Alaska households or the Alaska economy.

It’s not like the impact of the alternatives is difficult to identify. Using the data contained in ISER’s most recent (2026) assessment of the state’s fiscal options, we have included at the green dashed line in the last chart above, an estimate of the average tax rate that would have applied over the past decade if the state had expanded the tax base either through the use of a sales or income tax to include non-residents. Rather than the 3.63% average tax rate on Alaska AGI that was actually assessed on Alaska households, the average rate on Alaska households would have dropped to 3.05% on Alaska AGI.

The difference, which represents an annual average of approximately $175 million (or approximately $275 per PFD, or $750 per average Alaska household), would have put real money in Alaska families’ pockets. Instead, the Legislature chose to take that money out of Alaska families’ pockets so that non-residents could keep the same amount in theirs.

It seems hugely inconsistent to argue for “process” before imposing a long-discussed tax on a corporation, when the Legislature has continually ignored that step before imposing a tax, and subsequent repeated increases in that tax, on Alaskan households.

The difference in treatment reveals the real purpose of the “process” argument: to use it as another excuse to delay closing the S-corp loophole for as long as possible.

The intended effect is to protect corporations from paying taxes by far more than the Legislature has protected Alaskan households.